Disruptive innovation, blue ocean strategy, and 'jobs-to-be-done': implications to effective product management

Disruptive innovation, blue ocean strategy, and 'jobs-to-be-done': implications to effective product management

In this article, I'll break down three innovation-based frameworks and their implications to how product managers can design processes and cultures to unlock differentiation.

“If you don’t innovate, you die.” — this statement by Gary Vaynerchuck is representative of the state of business-building today. According to Bain, several decades ago, 95% of the valuation growth in the most successful companies over a 10-year period occurred by relentlessly pursuing one or two core businesses and pursuing adjacent markets. Today, what Bain defines as “Engine 2 businesses” (defined as new businesses with a strong, insurgent mission within a company) defines up to one-third of successful companies’ valuation growth in the same time period. Why is innovation suddenly so much more of an imperative compared to the past? To put it simply: cash / capital is more abundant than ever before, business boundaries (who customers are and why they value a particular market) are being increasingly being redefined by turbulence (hello COVID-19), and the ingredients to successful business-building are more available than ever before (due to software, brands, and intangible assets). It’s incredibly clear why successful innovation, and understanding how to harness it, is important to every business today. Innovation is defining every industry — from healthcare, to education, to finance, to government.

However, for the most part, innovation is an inaccessible buzzword. Its use in consulting research papers, books, and venture capital reports are anything but applicable to the modern day manager or worker aiming to understand how to utilize the theories of innovation in their day-to-day work. Having been an engineer in college, worked in digital investments in the Private Equity Group at Bain, building my own non-profit Cornerstone as a de-facto product leader and CEO, and now working as a product strategist at GovTech Education Indonesia — I sought to break down innovation practices from the best minds and turn them into applicable practices and mindsets, specifically for a modern day product manager. Innovation seems like this unpredictable beast, but in reality there are methods and processes that can be embedded to allow for replicable and consistent innovation to occur (which is why the best companies at this constantly innovate — think of Google). In this article, we’ll touch upon topics like “why objectively good management - e.g. listening to your customers - can be a bad thing”, “why cultures inside organizations matter and why even great cultures can limit innovation”, “why customers won’t buy an objectively better solution”. We’ll mainly touch upon the theories elaborated by 5 books: The Innovator’s Dilemma / Solution by Clayton Christensen, The Jobs to Be Done Playbook by Jim Kalbach, and Blue Ocean Strategy / Shift by Renee Mauborgne and W. Chan Kim. These theories will be amplified by my own personal experiences and perspectives, and I’ll follow up these theories with synthesis on applicable mindsets that product-related workers can utilize in their day to day work. Without further ado, let’s dig in.

Disruptive Innovation (The Innovator’s Dilemma and The Innovator’s Solution) and Jobs to Be Done

In The Innovator’s Dilemma, Christensen touches upon two types of innovation:

Sustained innovation: When businesses innovate and create value through the characteristics the “established market” values — especially for the most profitable customers. For instance, in the disk-drive industry, established customers valued the “highest capacity”. Thus, incumbent players would design processes within their company aligned to getting more and more capacity.

Disruptive innovation: When new technologies enable businesses to innovate on characteristics the established market has not yet valued, at the cost of “weaker value” on the what the established market values. Although the market likely starts off in a niche segment, the disruptive innovation is able to “catch up” to what the established market expects over time (thus disrupting the existing players) while capturing new customers.

The idea of disruptive innovation is that how incumbent businesses evolve and “what customers demand” actually align across two separate curves:

Naturally, incumbent firms will be drawn in the long term to the higher end of the market due to higher profitability (gross margins to be extracted) from the high end. However — while these customers would want to have higher product performance across established characteristics (in the graph above the line is flat but it’s actually angled upwards although at a less steep slope than the progress) — the incumbent firm is likely to make incremental progress that overshoots what is actually demanded. It’s really hard to assess what’s demanded so the best of the best firms will just try to push progress as much as possible whether it’s faster and faster speeds, capacity, memory, battery life, graphics, you name it.

Meanwhile, disruptive innovations start off in the low-end or a niche market. They are often overlooked by the incumbents because they are initially deemed unattractive by the current principles of the existing firm (we’ll touch upon that below). However, they often tend to be able to scale up to what existing customers demand eventually while offering new value that the previous product couldn’t — hence “disrupting” the old business models as they meet customer needs exactly where they are while offering differentiated value.

Christensen explains that large incumbent players struggle to create disruptive innovation because their value networks / cultures (exhibited by their resources, processes, and values — or RPV) are aimed towards sustained innovations that tend to result in overshooting customer’s value curves because that’s how the big players differentiate amongst their competitors (e.g. we make a hyper-quad dual 8GZ mega-bastion disk drive that’s 2% faster than all of our competitors).

Let me explain what these three terms are:

Resources: Their existing assets, capabilities, human resources, etc.

Processes: The standards that exist within the company in order to ensure consistency (e.g. the product development process, the rhythm that exists between sales, customer success, and product managers)

Values: The prioritization framework that a company utilizes to decide what matters to them and what does not matter to them

Within this framework, “good management” (aka a company listening to their customers, focusing on maximizing market share within their focus target markets, etc.) can actually result end up resulting in incumbent players failing to be able to react to disruptive opportunities. And this is not because they are incapable or blind to these opportunities, it’s that their “value networks” (the way they perceive value) is extremely different to what is needed to succeed in building up disruptive businesses. This is why there are more than a handful of examples of disruptive startups being grown out of employees who left incumbent companies (who probably spotted some of these opportunities when they were in their original companies). Let me give a few examples:

In “good management” we want to make sure that we’re maximizing our profitability (gross margins) and focus on the customers that generate this. When new technologies enable value across a different spectrum of “needs” but fail to generate the same level of profitability / value to the company — naturally the company will think that it’s not worth their time. By company, we don’t just mean leadership, but also the people within who are operating around the status quo cultures of the established company. For instance, salespeople might actively sabotage plans to sell a new product to their active customer bases because they don’t know how to sell something that “performs worse” across dimensions that they’re used to hyping up and potentially to a newer set of customers who are less profitable than their usual set (if you’re making $1M in profit a year, you’re not going to be excited by a new opportunity that only generates $20,000 at first).

In “good management” we also actively allocate resources to things that have strong expected value of working across factors that are easily measurable. For instance, BCG’s Growth Share matrix below highlights the prioritization framework that most companies use to assess whether to make investments. As seen, most companies (rightfully so) would over-index on “Star” (high growth, high market share) products and milk “Cash-Cows” to invest in “Question Marks” that potentially could have high market share in the future. However, the problem is that, with disruptive innovations, it’s really hard to know beforehand whether something will work or not / something will grow a lot or not. Rapid experimentation is necessary but most big companies are not great at mobilizing their existing processes to fit this need because of their existing value networks.

These resources, processes, and values are also the reason why acquisitions of companies that are made for their unique processes and values are best left alone rather than integrated into the existing company. An example of this is Amazon’s Zappos acquisition — which Jeff Bezos rightfully let “be” by their own right.

The implication is that because the value networks / cultures (RPV) are so deeply entrenched in incumbent companies — Clayton Christensen states that for disruptive innovations it is often better to set it up within a spin-off company / organization that can build up its own processes and values but also can tap into the unique assets and capabilities that the original organization has. At Bain, the successful “Engine 2” efforts had differentiated strengths in their “insurgency mindset, frontline obsession, and owners’s mindset”. This idea of a spin-off company is exactly aimed to build this by introducing the ability for the company to move fast, and be driven by its entrepreneurial spirit. In a $10M in profit company, a $20K deal might not seem like a big deal — but in a new organization, you’ll hustle and be scrappy with what you can get. You’ll build your R&D processes in a way that values and optimizes for the disruptive innovation’s needs rather than the existing market characteristics. However, critics of the spin-off organization idea cite that doing this is “often easier said than done” (as it does require significant resources and commitment to pull off to something that is at first experimental in nature). There are others who embed “innovation arms” into their pre-existing organizations — but then the critique of that is: “if you have an innovation arm, what does it say about the rest of the organization?” The truth is: the way you deal with disruptive innovation and sustained innovations is completely different. Understanding how to do both is absolutely critical, and not every innovation needs to be disruptive. Something like a spin-off company is an approach for disruptive innovation that should not be used for sustained innovation (as the existing RPV fits incremental progress already). But the spin-off organization may not always be the right answer. What if there were ways to build a culture that was adaptive and responsive to true customer needs?

OK — so we now we understand the theory of disruptive innovation and why it occurs. To sum up, disruptive innovation occurs when incumbent firms are zoned in on getting better at existing market characteristics and are “trapped” by their high-end customer bases who continuously demand the best of the best along those boundaries. These incumbent firms then tend to overshoot what the market demands and create a set of processes and values within their firm that keeps them doing that. Technologies that enable seemingly niche use cases at first pop up and are “too small” and “too weak” (along normal market characteristics) for these incumbent businesses to care about, until one day they’re not and are able to match what the market demands even for the high-end customers while enabling new use cases. The old “way of doing things” is thus disrupted.

What is the implication for a modern day product organization / manager? The answer lies in three things:

Investing in a culture and people / leaders who are focused on continuous learning vs. past track records — especially for venture building

Harnessing the “jobs to be done” vs. simply looking at existing market archetypes and making it better alongside regular market boundaries

Regularly experiment (make calculated bets) as part of the inherent culture and DNA of your organization and be patient for growth to occur while being impatient for profit

Let’s dig into these three implications:

First is investing in people who are driven to learn continuously vs. those who have stellar past records especially in stable industries. Regularly, those appointed to run new-growth businesses are people with the “right stuff” and a string of previous successes — assuming that more success will be in store. I see this in front of me all the time — when venture capital firms in Southeast Asia without question get hot and heavy to invest in ex-MBB or ex-IB folk. Sure, they’ve shown that they probably have strong intellectual prowess and capabilities and ability to be “professional”. However, these are a completely different set of ingredients necessary in order to be successful in launching a new venture. In How Google Works, past executives Eric Schmidt and Jonathan Rosenberg detail how innovation and hiring works at Google. I highlight two quotes below:

“Henry Ford said that ‘anyone who stops learning is old, whether at twenty or eighty. Anyone who keeps learning stays young. The greatest thing in life is to keep your mind young.’ Our ideal candidates are the ones who prefer roller coasters, the ones who keep learning. These ‘learning animals’ have the smarts to handle massive change and the character to love it.”

“Product development has become a faster, more flexible process, where radically better products don’t stand on the shoulders of giants, but on the shoulders of lots of iterations. The basis for success then, and for continual product excellence, is speed.”

Managers who have progressed through stable business units will have developed skills for those scenarios: operational management, process improvement, strategic analysis for existing markets, cost-controlling, and so on. I saw this when I was in consulting, with the pinnacle of the “we know what the right way is and we’re going to follow it no matter what” being the McKinsey Way: a unified mindset of how they approach problem solving. In fact, the McKinsey Way is so integrated and standardized into the DNA that a McKinsey Associate from Indonesia will have eerily similar “ways of working” as a McKinsey Associate from North America. At Bain, I saw this in my day to day work. In as many situations as possible — we rehashed problem solving methodologies from old cases — and had the mindset that “cracking the case” was the most important thing. I remember that a Partner saying: “Don’t question — just do what you’re told”, and another writing down in his kick-off deck: “Don’t be a stress multiplier!” However, as we can see from disruptive innovations, it’s impossible to predict from when and where these innovations will come from and hence “stress” is sometimes going to be needed (writing something like this reduces the desire for people under to feel like risk is something that is warranted to have — although I know the intent was probably to just signal to people to check their work and meticulous). One of my friends, Koray Koska, a founder of an early-stage FinTech company at 22 said to be (and this stuck with me): “I didn’t know a thing about credit cards or FinTech before I started — but I kept going, and going, and going until it led me somewhere”. Out of all of my friends who have had some form of success in building early startups — from Sheridan Clayborne, to Naga Tan, to Wafa Taftazani — the ingredients that lay the foundation for their success was never their past experiences (and they’ll tell you this) but rather their unending curiosity and hunger to fail, adapt, and learn.

For a modern day product manager, the implications of this are clear. It is important to build a culture where hiring talent, training talent, and daily operations come from a place of deep learning and continuous improvement. It is important that “learning and challenging each other to be better” rather than the “status quo” is what is at the forefront of where the energy goes. Here are some examples that touch upon this:

Hiring talent: Top tech organizations hiring people without even any college pedigrees for the highest paying software engineering roles as long as they’ve demonstrated the chops from other areas. This is especially true for Web3 companies who are paying top dollar for scrappy, hungry talent.

Training talent: ServiceTitan, a scale-up I interned with, pays for everyone’s LinkedIn Learning subscriptions and encourages everyone to share what they’ve learned with each other amongst their teams and groups

Daily operations: Introduce a writing culture (something my boss Rangga Husnaprawira is especially fond of) when making decisions thus embedding a culture of questioning, learning, and addressing counterarguments on paper in long, narrative format. This is founded upon Amazon’s writing narratives vs. decks (which don’t capture the nuances in decision-making and thus leaves things to improper interpretation)

Second is investing in thinking about “jobs-to-be-done'“ vs. just making things better for our specific market archetypes (e.g. optimizing things for millennials, or our big customers). Remember that disruptive innovations end up occurring between incumbents overshoot for what the market demands due to inertia and the value networks / culture they’ve created, and thus creates an opportunity for an at-first niche player to shoot up with differentiated value add. You might ask — isn’t a solution to this for an incumbent to always be in tune with what a customer demands? The answer is yes — but it’s not as simple as you think — highlighted below (from The Jobs to be Done Playbook):

“Jobs don’t come in neat little packages. You have to hunt for them. You won’t find jobs from analytics or surveys, and you can’t just brainstorm jobs and needs. You have to get out and talk to job performers in formal interviews — lots and lots of them”

So what are jobs and why is understanding them one of the solutions to the Innovator’s Dilemma? Jobs are the underlying needs and objectives of why people do the things that they do vs. how organizations usually analyze (which is by packaged demographic or psychographic characteristics). There are four principles to the JTBD framework:

People employ products and services to get their job done

Jobs are stable over time through technological change

People seek services that help them get their job done faster and easier

Making the job the unit of analysis makes innovation more predictable

To sum it up — while the Innovator’s Dilemma mentioned that technological innovation introduced the opportunity for disruptive innovation to happen — the truth is the reason why these disruptive innovations really had a foothold to disrupt is because they eventually captured the underlying job to be done rather than constantly trying to advance on defined characteristics.

Here’s an example of a job: Mary is a 27-year old professional in Jakarta, waking up early in the morning to workout in Crossfit 6221 and then rushing back home to get ready before getting to work online. She enjoys getting a sense of what’s happening in the world — but usually doesn’t have time for anything long, and is not really a big fan of multitasking (e.g. listening to a podcast while working). She probably has 10-15 minutes max while drinking her coffee to get her news fix in — but it’s annoying because there are too many curated newsletters out there (that’s ironic), too many topics of interest, and it often takes 10-15 minutes to find just what she wants to read. Thus, the job Mary is trying to get done is: (1) finding good-enough news that’s relevant and personalized in the right way for her, and (2) fitting and reading that all in a 10-15 minute window. Solutions that just focus on getting the best news, curating great content but making it not easily accessible / readable — are not going to solve Mary’s underlying job. I don’t know what the right solution is (and I’m sure many have been proposed), but the insight to that 10-15 minute window of personalization while Mary was drinking her pre-coffee work is an insight you can only get from speaking to her. And if enough people echo similar types of insights, you start to form a sense of a potential business model that can scale and work.

What are the implications of this for product managers: it’s simple, you must continuously hunt to more deeply understand the customers’ lives. Chances are — you’re not the intended customer of the product you own — and in fact your daily lives and mentalities may be vastly disparate from your customers. My professor at Kellogg, Kevin McTigue used to always say: “Just by nature of being at Kellogg — you’re weird! If you’re handling a mass consumer product, you are not your customer and you need to step out of that mindset by actually talking to your customers as opposed to just brainstorming in your little ivory tower.” Marty Cagan, in his book Inspired, also writes the following about the importance of speaking to customers on an extremely frequent basis (he recommends that even if product managers are not intentionally trying to discover something, there should at least be 2 hours of customer speaking done per week):

“One of the most common traps in product is to believe we can anticipate our customer's actual response to our product (based on customer research or our own experiences). We MUST validate our actual ideas on real users and customers - we need to do this before we spend the time and expense to build an actual product and not after.”

For product managers in all organizations — not just those in disruptive ones — it is critical to build the muscle and the habit of speaking to customers on a continuous basis. If this is not the culture of the organization, make it your own personal mission and do it yourself if needed. I guarantee that sharing this level of detail and continuous insight to the organization will differentiate you tremendously, and allow you to be able to realize breakthrough ideas (that might be simple and right in front of your face had you taken the time to do this).

The third implication for product managers is to conduct regular experiments (calculated bets) with patience for growth and impatience for profit / value. One of the things we know in disruptive innovation is that it is impossible to really predict with an absolutely certain precision level what will work. In this case, continuous experimentation is necessary with the mindset that "not all ideas will work — and that’s okay”. Oftentimes, existing incumbents without this mindset will fear experimentation and over-index on trying to predict the outcomes of the experiment (financial models, etc. — saw this again when working with clients at Bain) which is where startups are able to move with a lot more mobility.

It’s important to note that regular and consistent experimentation doesn’t necessarily mean launching an entire product while “spraying and praying”. The Discovery process in effective product management is exactly aiming to build a systematized way to ideate and test ideas in a rapid way (according to Marty Cagan — the best organizations at this can test as much as 10-15 ideas in a week). To do this, product managers must build skillsets in intentional prototyping and experimentation. Many product managers associate prototyping with “usability tests” or “ensuring that engineering can build the features” but it is actually possible to test for value (which is an indicator of potential growth). Here are a few examples of ways to do this even before you commit to developing the products itself:

Testing value quantitatively: Build a live-data prototype to prove that certain features can work and that users are getting value out of what you’re building (e.g. A/B tests, Wizard of Oz prototypes, bootstraps e.g. when Reddit launched all the founders literally bootstrapped all of the articles in it so it seemed “full”)

Testing value qualitatively: At the end of a usability interview with a customer, get a “commitment to buy” from them in a verbal way. Ask them if they’d recommend you to their friends and make them send an e-mail to them on the spot. Ask them if they’d be willing to schedule significant time with you to discuss. These are all ways to test value before you commit to building something

Testing demand: Setting up a “fake door” demand test by making it seem like a feature is already launched (e.g. let’s say you set up a post on your brands’ Instagram page) and having a button where they can go and check it out. When they check it out they go to a page where you can track analytics, and gather user information through things like e-mails when it actually launches

The point is — many product managers do not experiment as much as they should and have not build up the skillset to do experiments in a way that tests value reliably, consistently, and rapidly. This muscle of experimentation in something that can immediately differentiate an effective product manager from one who’s not.

Now let’s talk about having patience for growth while having impatience for profit. As the Innovator’s Dilemma highlighted — incumbent firms find it hard to invest in anything that does not grow to a level that is “meaningful” to them (if they’re already big — a new venture that is 0.5% of their revenue is hard to be excited about). However, growth takes time (disruptive innovations start off small by nature). Thus, it’s necessary to be patient with this. However, at the same time, it is important to be impatient for profit and value-creation (of which was highlighted above). Google states this well:

“When you want to spur innovation, the worse thing you can do is overfund it. As Frank Lloyd Wright once observed, ‘The human race built most nobly when limitations were greatest.’”

Helping out a new growth / disruptive business with too many resources from the core is not the most beneficial because it won’t be scrappy to win. It’s something I felt deeply having founded by own business. As a modern product manager, what this means is to focus on value-creation and building out profits from the very beginning instead of waiting until later to do it.

Blue Ocean Strategy

The next framework to touch upon is Blue Ocean Strategy — which details another theory of innovation that is similar, but also remarkably distinct from disruptive innovation. Like disruptive innovation — the aim is to build a replicable process and framework of innovation. However, unlike disruptive innovation, the focus is not to necessarily “disrupt” but to “create” in a blue ocean of unexplored opportunities and potential. Instead of swimming in a bloody, red ocean of competition that ultimately results in lower, lower, and lower margin and a race for market share — the goal of an effective blue ocean strategy is to build the mindset and toolkits to understand how to “play in your own zone” and unlock value from previous non-customers that are looking for value amongst completely different definitions than the traditional market. The core similarity between this and the disruptive innovation framework is the fact that it should be all about the value that is created vs. focusing solely on pre-existing market boundaries.

The funny thing — this type of competitive differentiation in theory is understood by every strategist and product manager. However, in practice, the way that strategists build up an understanding of competitive differentiation is always within traditional market definitions. They map out technical comparison perspectives to benchmark against competitors, but then fall into the trap of building “me too” businesses that in reality differ only in “incremental progress” from the rest of the competitors but actually are not very different across things that customers actually value. Let me highlight an example from the book Blue Ocean Shift highlighting a company called School Foods that was marking where it stood amongst competitors:

“After discussing their factors of competition, the team began to plot their strategic profile against the two dominant rivals. The strategic profiles of all three converged along the same dimensions of competition: financial accountability, quality of management services, transparency of bidding processes, and the like. The only difference was that the two industry leaders had higher name recognition, whereas School Foods had a high sense of mission. The team was probed: “Do any of your customers know that you value your sense of mission?” “No, not really… I guess not,” a team member reluctantly replied. Upon reflection and discussion, the team then agreed: They might be proud of their mission, but customers were clueless about it.

“Do you know what your competitors have to offer in terms of food, quality of service, or ambience?” a blue ocean expert asked. The entire team went quiet. There were blank faces all around. Eventually, a team member responded, “No, we don’t really know what they offer, nor do we really know how our food offering is valued versus theirs by our customers.” The probing then went deeper: “Why isn’t the quality of food or variety in the offering noted as one of your factors of competition? You are a food-service company after all, aren’t you?” The group was amused, but ashamed. “I guess we are so focused on winning the bid to provide the service by offering the best financial package desired by the management of the school,” one team member confessed.”

It doesn’t always go this way — but the truth is oftentimes competitive differentiation analysis is done in a way that highlights our strengths and how we define the market to be rather than what customers value the products to be. I saw this at Bain — when I was speaking to industry experts about how they saw the strategic profiles of the market to look like. Let’s take an e-commerce example: horizontal e-commerce players in Indonesia such as Shopee, Tokopedia, Bukalapak all talk about the same things: price, discounts, delivery SLAs, geographic range, # of merchants, diversity of product offerings, UI/UX, etc. From an objective perspective, besides marginal differences, they’re all really doing the same thing (mostly the differences are based on perception — e.g. Shopee has more discounts but Tokopedia, but is this REALLY true?). And strategic differences are minimal. Yes, Bukalapak might say they’re differentiated in terms of their focus on MSME’s — but let’s be real, how much of this is spurred by a top-down desire to differentiate their story vs. an actual differentiation based on real and genuine customer value? On the other-hand, quick-commerce players such as Astro (not saying that I’m bullish on this business model), make the trade-off of traditional market characteristics such as geographic range and price — and focus on what they found their customers (both previous e-commerce customers and also non-customers) really value: delivery speed and high quality. They are willing to make trade-offs to other factors in order to focus on these two characteristics.

The core of blue ocean strategy is exactly that: what trade-offs do we have to make to be able to focus 110% on the things that may unlock non-customers to buy or “almost non-customers” to switch. It’s highlighted by this framework below from Blue Ocean Strategy / Shift:

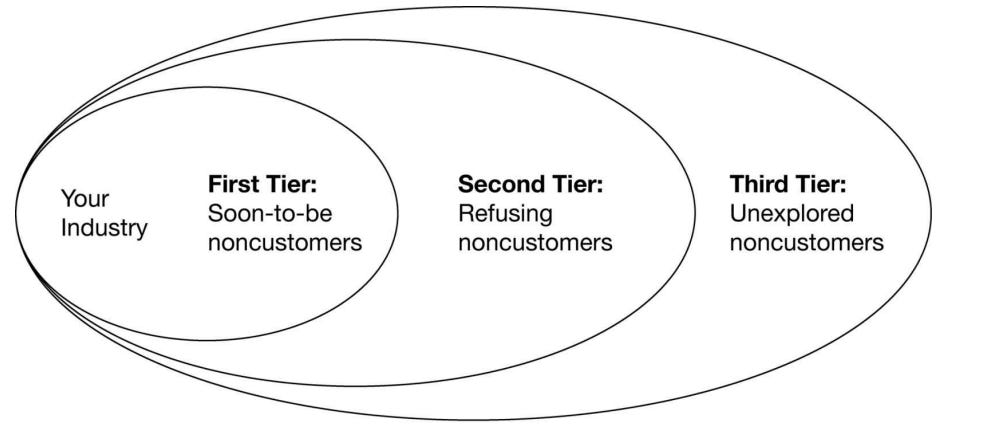

As we can see by the four different actions (Eliminate, Reduce, Raise, Create) that can be taken to unlock true blue-ocean differentiation — it all comes down to drawing a new “way” to view the market. Instead of focusing on only zoning to existing customers and listening to what they need (which similar to disruptive innovation pushes you to pursue more and more things and potentially overshoot in the characteristics that lead you to red oceans of competitive bloodbaths) — blue ocean strategy encourages to think about our “non-customers” across different frontiers. These groups of non-customers are the exhibited by the following graph:

These non-customers are explained as the following:

First tier: Soon-to-be non-customers are on the edge of the industry, waiting to jump ship as long as a better solution that fits their needs comes. Think of the credit card industry, where small and medium sized merchants tolerate the cost of installing POS systems and the fees associated with each swipe simply because there was no better solution in the past

Second tier: Refusing non-customers consider your industry and consciously choose to not choose it (e.g. because of price or because another industry solves their problem better). In the credit card industry, these are micro-businesses who choose not to install POS systems and opt for cash (I see this in Indonesia a lot where it’s just not worth it for some merchants; some have them but set minimum basket sizes due to the transaction fees)

Third tier: Unexplored non-customers are currently in seemingly different markets. This is not “everyone else” (it’s not MECE) and it’s important to understand the difference between that. An example is in this credit card market is POS systems for individuals. Before Square / Venmo, the assumption was that “a transaction had to involve a merchant”. For individuals, they reluctantly went to an ATM to withdraw cash to transfer money to each other

The goal of blue ocean strategy is really is to understand how we get to these tiers of current non-customers. By doing so, potential markets can be tapped into that capture a large size of the pie beyond what has been captured before. As Clayton Christensen mentioned with disruptive innovation, first mover advantage in these types of “new industries and new markets” is incredibly powerful. By understanding how to do this systematically, product managers and business strategists both can tap into a different paradigm of success and growth.

There are three main implications of blue ocean strategy for effective product managers:

Deeply challenge your assumptions of what people value (by talking to actual people on the ground even beyond your current customers!) and deeply understand where you stand today amongst the competitive landscape

Understand how value is created amongst not just immediate competitors but also amongst adjacencies to the industry to draw inspiration

Develop a way to systematically test this within the organization — going against the grain and a culture that is intrinsically “red ocean focused”

The first implication is deeply challenging your assumptions of what people value and deeply understanding where you stand today amongst the competitive landscape. Both are inter-tangled because your assumptions of the world around allow you to map an honest picture of what the true competitive benchmarks actually are (vs. based on your own or on your company’s own worldview). And as my co-worker and influencer Budi Tanrim says: “A good product manager knows how to be customer-centric. A great product manager deeply understands the competition.”

The only way you can properly challenge your own assumptions is to (1) recognize them, and (2) talk to actual people to understand the fundamental truth (this is very similar to what we talked about in the disruptive innovation section). How you recognize your assumptions (and hey this skill also applies to your personal life) is by walking through your own mental models for how your industry works as you know it. I like to draw and visualize things like how customers come to choose a particular solution over others. How did they come to that decision? How did they discover it? I want to really nail down and understand — as I see it — how things work. Then, by talking to actual people on how they accomplish a particular “functional task” (remember the job to be done framework?) — how do they do this in practice? I bring my assumptions to the table to make it clear for them where I think the picture is and get them to help me correct my mental model. I’ve used this skill over and over and over again in my job as a founder at Cornerstone and am bringing this practice over to how I’m building a “Product Ops” product at my job at GovTech Education.

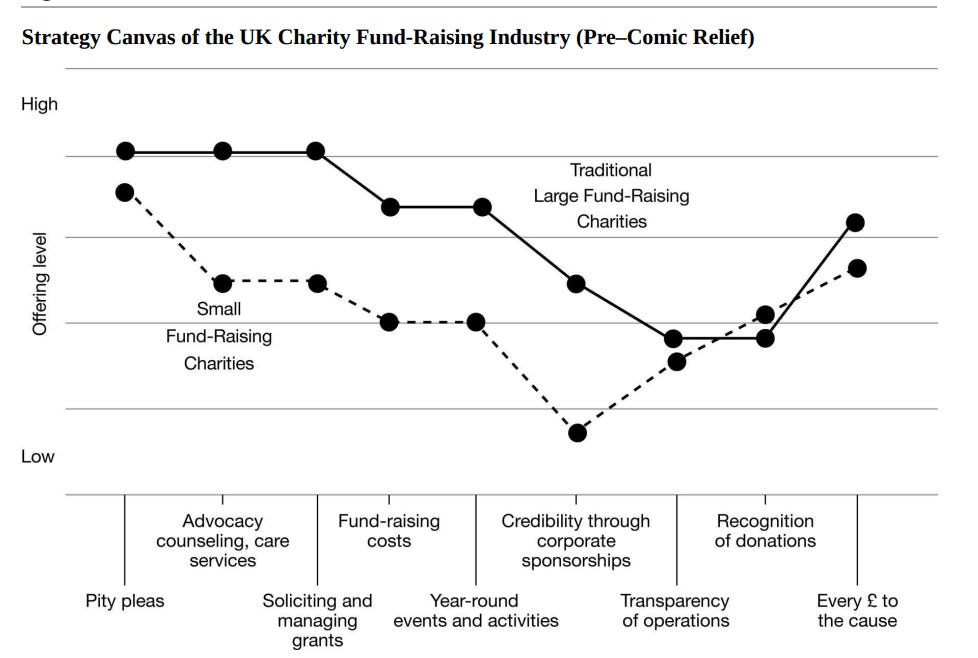

Then, when you understand your own assumptions and thus start to have a more clear picture of how the world and competitive landscape actually works — you then map it out to have a sense of where you really fall within the competitive picture (only choose 1-2 main competitors at max). Here’s an example of the UK charity system:

More often than not — you’ll start to notice that the market boundaries between competitors are often played on similar lines. Sure, there might be take and give and one competitors may be better than the other on certain things and vice versa — but the curves tend to converge in a similar shape. This is indicative of a red ocean, and an opportunity for blue oceans to shape. In the case of the UK charity industry — what was realized was that many of these attributes were taken “for granted”. Charities “had to” solicit and manage grants while running year-round activities, focused mainly on high-end donors through their solicitation operations, and creating marketing strategies by tapping into the image of the “destitute poor who needed help”. All of them were organized in this way, and hence it was impossible to differentiate in a significant way. Now in came a charity called Comic Relief that challenged the assumptions of the traditional industry and came in like this:

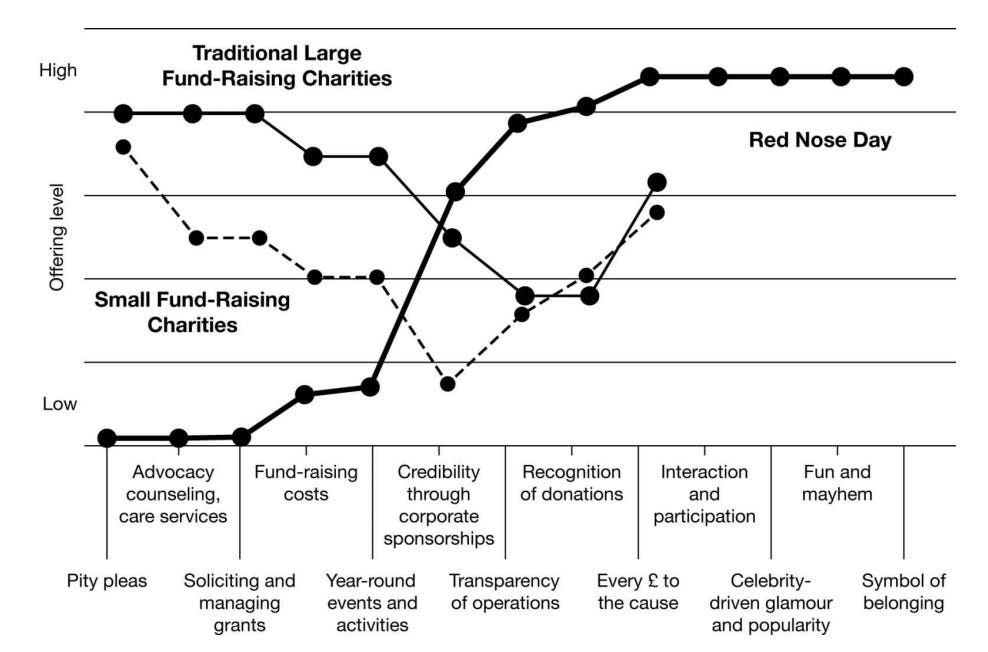

Using the Eliminate-Reduce-Raise-Create framework we introduced in the start of this article, we can see where Comic Relief made an action to completely differentiate from how competitors organized themselves. They completely eliminated the “pity pleas” (aka appealing to people’s sense of pity) and introduced a charity marketing campaign that was all about community and fun. They reduced solicitations and year-round events by creating an event that only happens once every two years, and works with multiple retail stores (e.g toy stores) vs. their own solicitors in the UK to organize fundraising thereby focusing on mass donors vs. just the high-net-worth individuals. In addition, they raised the bar on transparency, recognition of donations — while creating new value in interaction / celebrity-involvement / and symbol of fun and belonging. Because they were so different than their competitors and were able to save costs through eliminating / reduce functions that are unneeded — they were able to focus 110% on building their own value curve. This is for sure an easier said job than done — which leads us to our second implication.

Our second implication is to draw inspiration not just from immediate competitors but also from adjacencies. By mapping out and drawing how customers obtain value from various adjacent sources (e.g. substitutes, throughout the chain of usage, etc.) we get to obtain inspiration for the ideal design of our product and where we can draw out new value curves. Understanding these also makes you a more knowledgeable product manager overall. These six adjacencies include:

Alternative industries: Look at alternative industries that serve the same function or solve the same problem, but that have a different form. Choose the alternative industry that attracts the most customers. What are the decisive positive sources of value and the detractors of value that make people gravitate to and choose one alternative over another?

Strategic groups within the industry: Look at alternative strategic groups (e.g. across price categories like 3-star to 4-star to 5-star hotels). Why did buyers trade up for one strategic group and trade down for another? Focus on identifying the distinguishing factors that made them choose one strategic group over the others.

Look across buyer groups within the industry: Look at buyer groups that exist within the industry. The main buyer is not necessarily going to be the main user or the influencer of the product. For instance, when you’re selling a B2B product, you might be focused on corporate purchasers who evaluate things on a one-off basis. But what about getting the CFO’s buy-in that see the larger picture of the costs and how it played out in the long run? If you’re selling a product in retail - are you thinking about offering a leap of value to the influencers (who might be the retail staff in the stores)?

Complementary / service offerings: Look at what happens before, during, and after the product is used. Do you notice any particular pain points that exist? Understanding the full context is very important to delivering the value that enables the customer to perform their “job”.

Functional-emotional orientation of the industry: Probe to understand whether an industry is predominantly seen as “functional” or “emotional”, then flip it around to see what it could look like to be the other way. Let’s take the legal profession for example. Lawyers are seen as a functional service - but what if it was turned the other way to something that appealed to the emotions (e.g. of support, of care and empathy). Supermarkets are seen as functional, but if they’re seen as fun and an experience?

Shaping external trends over time: What are the main decisive, irreversible trends that will shape the industry in the future? Anticipating these — what are ways that you can offer a leap of value that allows you to shape how the trend ends up evolving?

As you can see — by focusing not only on direct competitors but being very comfortable and getting inspiration from the full context of “what customers see” — you’re often able to find breakthrough ideas where value can be added and where certain assumptions that one holds starts to fall flat when only assessing from a single-minded perspective.

Our third implication is to develop a way to systematically test these processes within the organization — going against the grain and a culture that is intrinsically “red ocean focused”. The truth is doing all this work to assess blue ocean opportunities is not necessarily “insanely difficult” but requires a lot of work. However, everyone’s busy in the organization. No one really has the time to add this on top of their already stacked responsibilities. Thus, when doing this type of “blue ocean strategy” work-stream, the implication is that it’s less so something that is a continuous “mindset shift” as with the case of the Disruptive Innovation learnings. For a product manager / product leader, setting aside a “sprint period” (potentially 1-2 weeks of intense, intentional work) where there’s the intention to really extract insights from this type of work can yield strong results. The insights can then be shared across the Product organization, and be utilized in iterative workshops.

But it doesn’t just have to be relegated to a sprint work. As a product manager, developing the insights from the full context of work over time and building your repertoire of understanding along these lines (most product managers would just look at existing customers only) will make you a stronger business leader with the ability to “see” in innovative ways. If you have the time to do this extra bit of research — it could be a great way for you to stand out and offer differentiated value / insights (even if it takes a bit of time, energy, and work to do).

Conclusion

With this article — you’ve learnt what innovation means beyond just theory, and hopefully have gained some inspiration on how to apply it to your day to day job in product in an applied manner.

From Disruptive Innovation, you’ve learned to think from a “jobs-to-be-done” perspective, you’ve learned to invest in a culture / people that are learning-focused and adaptive vs. focusing on prestige, and you’ve learned the power of continuous experimentation.

From Blue Ocean Strategy, you’ve learned to be a great product manager that not only understands the current customers, but deeply understands how to challenge assumptions, map out the competitive landscape, and understand what the customer “sees” beyond just the “taken-for-granted” industry. All of these allow a product manager to offer differentiated insights and value — in a seemingly simple way.

I hope you find these helpful! If it did and you’d like to follow for more articles on product strategy, Indonesian entrepreneurship, and introspection / life planning — please subscribe to my Substack and follow me on LinkedIn :) Lots to come!