Do you know your credit score? A primer on Indonesia's credit data system (SLIK OJK, Credit Bureaus, and Skorlife)

Do you know your credit score? A primer on Indonesia's credit data system (SLIK OJK, Credit Bureaus, and Skorlife)

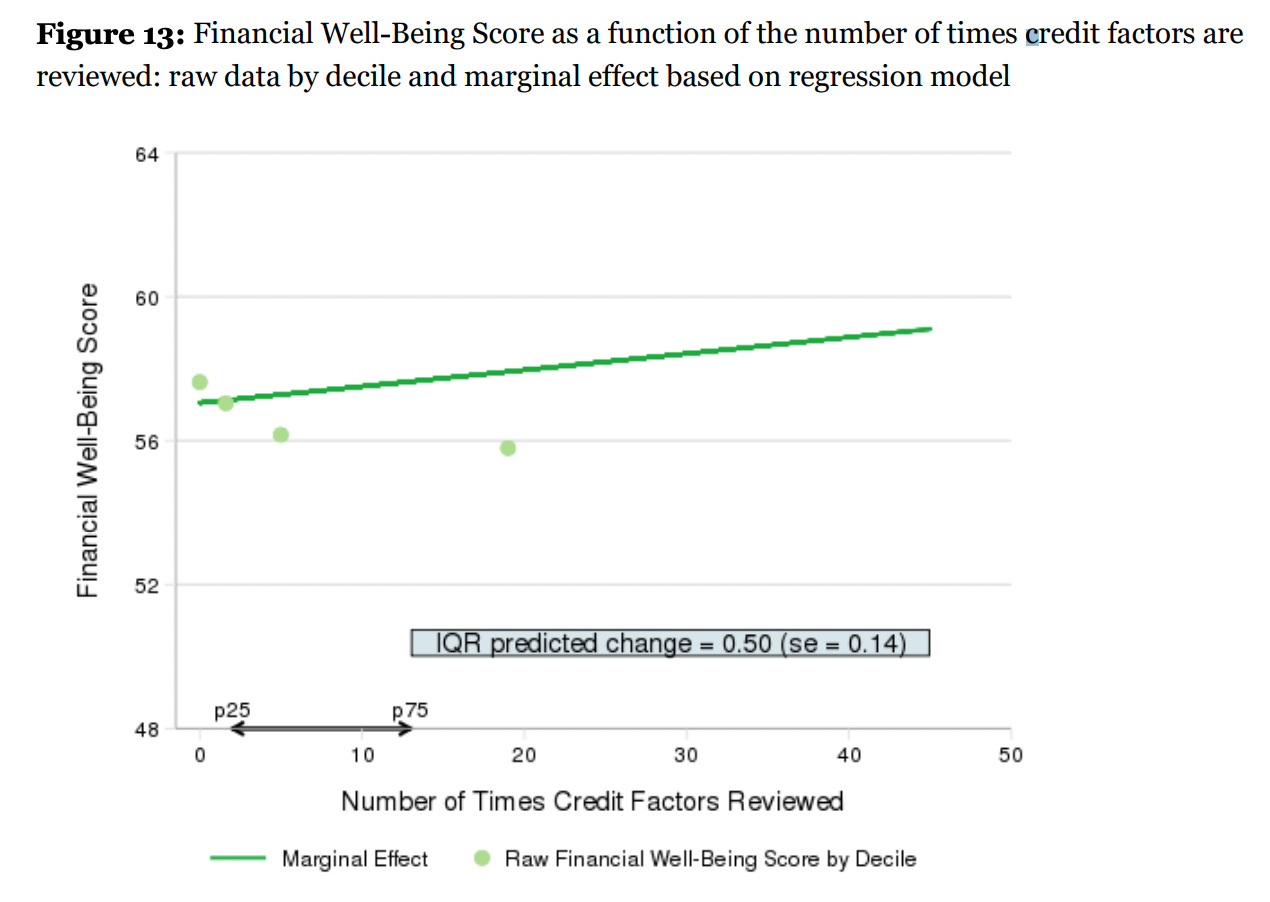

Consumers in developing markets like the US, UK, and India have largely been educated about the role credit scores play in their financial lives — to a largely positive effect. In the US for instance, credit scoring platform Credit Karma has more than 120 million users and has catalyzed a material change in consumer awareness of credit scoring. In a report done by the Consumer Financial Protection Bureau, research was done that showed a significant positive correlation shown between the number of times people reviewed their credit reports and people’s ability to pay debt (lower missed payments, less times in delinquency).

Credit bureaus have existed for quite some time in these markets (in the US, starting all the way back in the 19th century as local services to help local merchants determine which customers were creditworthy, even with a standardized scoring system called FICO that all the bureaus use in place). Even in India where only ~400M of the population of 1.5B have a credit report — the first credit bureau CIBIL began operations decently far back in 2000. People generally know the concept behind a credit score, and the importance of maintaining “good credit”.

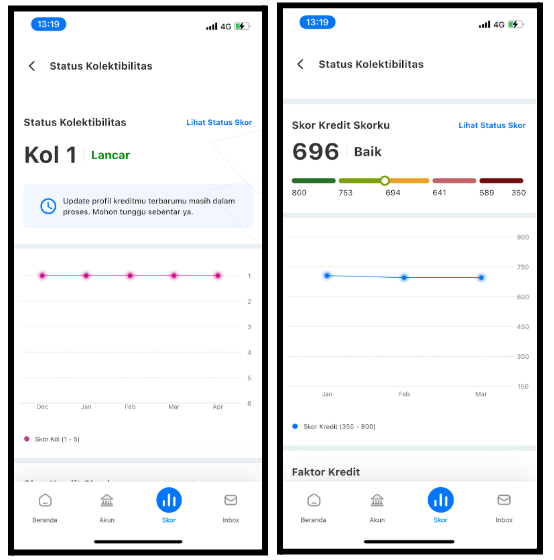

However in Indonesia if you ask a room of 10 people the question: “Do you know your official credit standing?”, the probability of someone knowing is very low. I’ve experimented with asking this question personally in a few different social groups, and at most 1-2 people would affirm their knowledge. And largely, if so, it’s a byproduct of chance or circumstance: in one case, a person got insight on their credit standing (specifically their “BI Checking” or collectibility score, which I’ll detail later) through a friend who worked at a bank. In another, the person was an employee at a bank and thus had direct access to pull their data. Another common scenario is someone getting rejected for a loan, and at that point in time being notified that their credit standing was bad — thus building the desire for them to check.

Point blank, if financial literacy is low in Indonesia (a survey that the financial regulator OJK did in 2022 revealed that five out of ten individuals were not financially literate), then credit literacy is probably markedly lower than that — especially in a country where formal credit access is also very low. According to a JP Morgan E-Commerce Report in 2020, credit card penetration was roughly 0.06 cards per capita (and the total number of credit cards in the country has stayed stagnant at around the 16-17 million range for the past 5 years). And yet, it makes sense, compared to the US, UK, and India (which have 99%, 97%, and >80% of their populations banked), Indonesia’s banked population stands at only 50% (the world’s third-largest unbanked population according to the World Economic Forum).

I. The formal credit reporting / furnishing system in Indonesia

On top of low formal credit access affecting credit literacy, the scaled provisioning and availability of accessing “credit data” for consumers has only existed in Indonesia in the past few years. The first credit bureau PEFINDO in Indonesia was only given its first operational license in 2015. However, before we go into this, it’s probably important to understand how credit data is furnished (or “supplied”) in Indonesia.

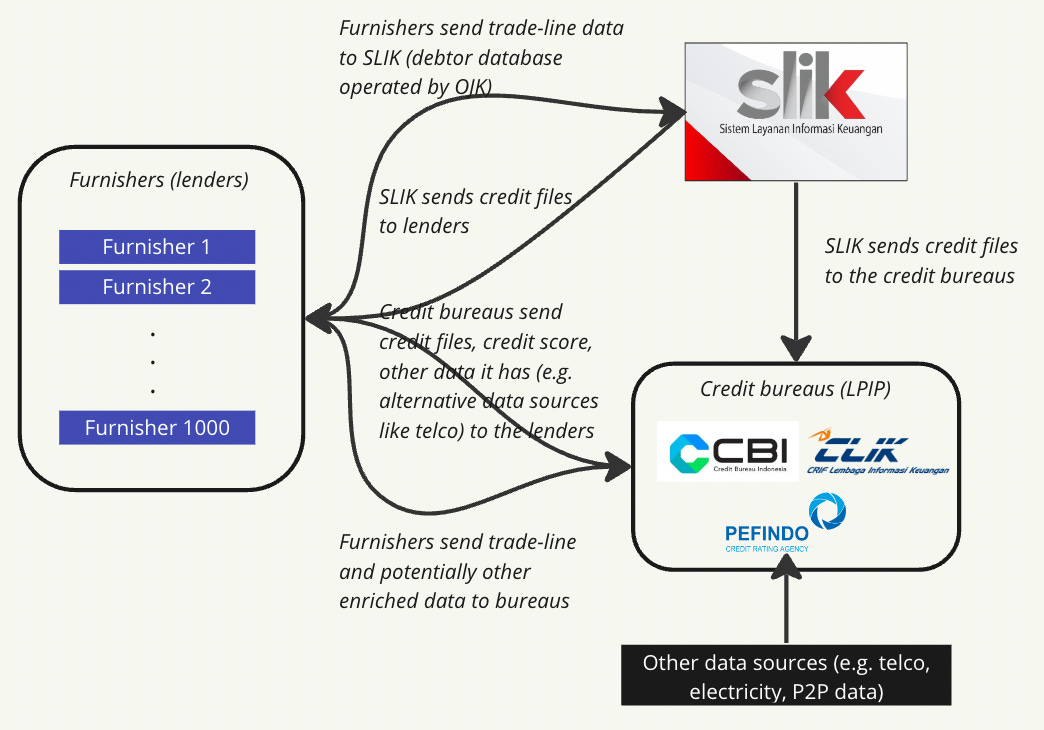

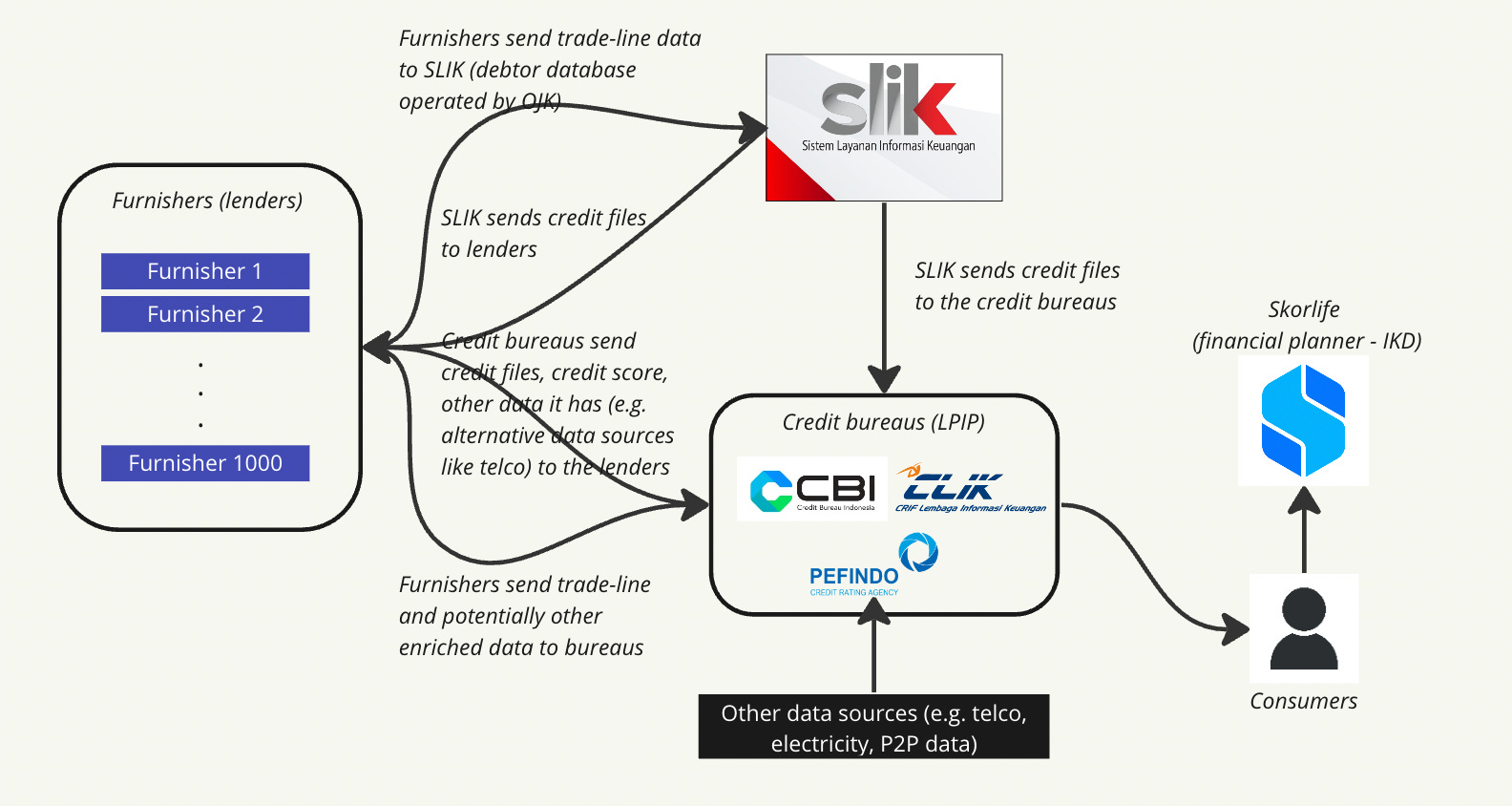

The diagram above summarizes how the major puzzle pieces of the credit scoring ecosystem fit together in Indonesia. Unlike most other countries, trade-line data (credit score parlance for loan data) is centralized at the national level under the financial regulator OJK — who owns a debtor database called SLIK (built in 2006). Furnishers (typically lenders) “furnish” data to the credit bureaus. The mandated furnishers to SLIK include banks (both conventional and syariah) as well as multi-finance institutions. It’s optional for P2Ps, cooperatives, and micro-finance institutions to report to SLIK. There are >2,000 such furnishers recorded in the database, and ~70 million people with credit reports in the system.

The furnished data is essentially a list of all the loan/credit accounts that the lender holds, with information on the borrower, outstanding balance, repayments and late payments, collectibility score (previously known as BI Checking), and other details for each account. This trade-line data is typically furnished to SLIK on a monthly basis.

The SLIK database is then tapped into by both lenders and the credit bureaus. Lenders can directly request debtor data from SLIK to assess customer’s creditworthiness. And the credit bureaus (called LPIPs in Indonesia) can pull this debtor data alongside other data it obtains independently (e.g. through furnishers who are not mandated by OJK to report to SLIK, enhanced data by creating its own partnerships with financial institutions, or alternative data such as P2P or telco data) in order to provide enhanced and more comprehensive data services — including credit scoring which SLIK does not provide.

The split is then clear: SLIK holds the vast majority of the universe of formal credit data. Credit bureaus then (a) tap into SLIK and other data sources it obtains through its own partnerships, and (b) utilize its analytical competencies (e.g. credit-scoring) to offer lenders a more comprehensive view of their creditworthiness. Unlike the US for instance, there is no standardized scoring methodology like FICO. Each bureau has their own way of calculating consumer’s credit scores — and the assessments could vary noticeably. In CBI I could be labeled as “great” while in CLIK I could be marked as “moderate”. For a lender, this could be confusing. That’s why generally speaking, the role of a credit score in Indonesia even to lenders is still not that robust. On top of this, the majority of bureau data today is that of SLIK’s, meaning that there’s still a long way for credit bureaus in Indonesia to mature.

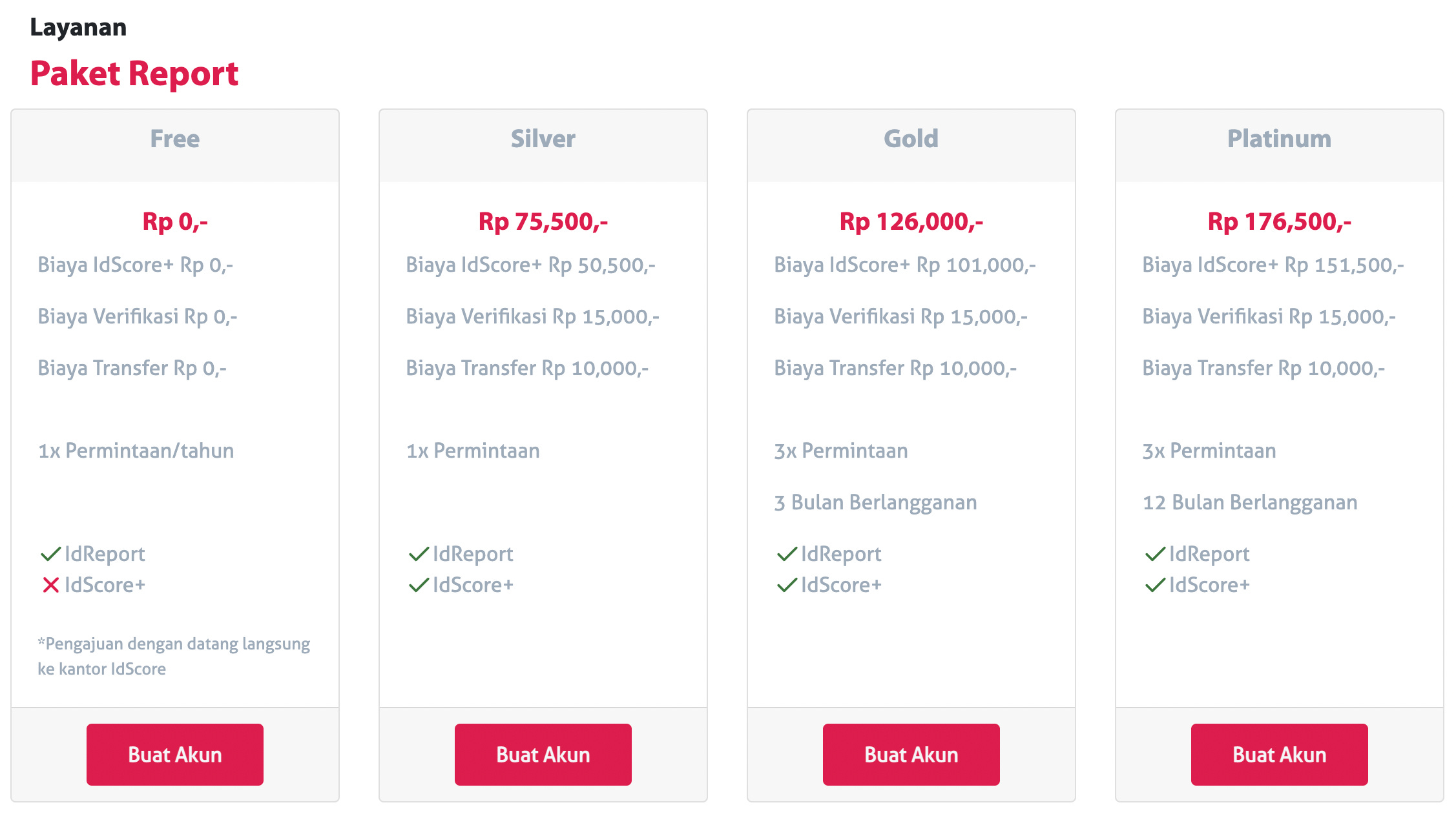

There are currently three credit bureaus in Indonesia (PEFINDO, CLIK, and CBI) — with the bureaus historically focused mostly on their B2B businesses. The only consumer solution provided by the bureaus currently is PEFINDO’s IdScore, a web-based solution that allows consumers to directly check their credit report. However, one has to pay RP. 75.5K (roughly ~$5 USD) to get this report, and the free once-a-year option requires users to go directly to the office of the credit bureau to obtain, which is located in Jakarta (a city with only 10 million out of Indonesia’s 273 million people).

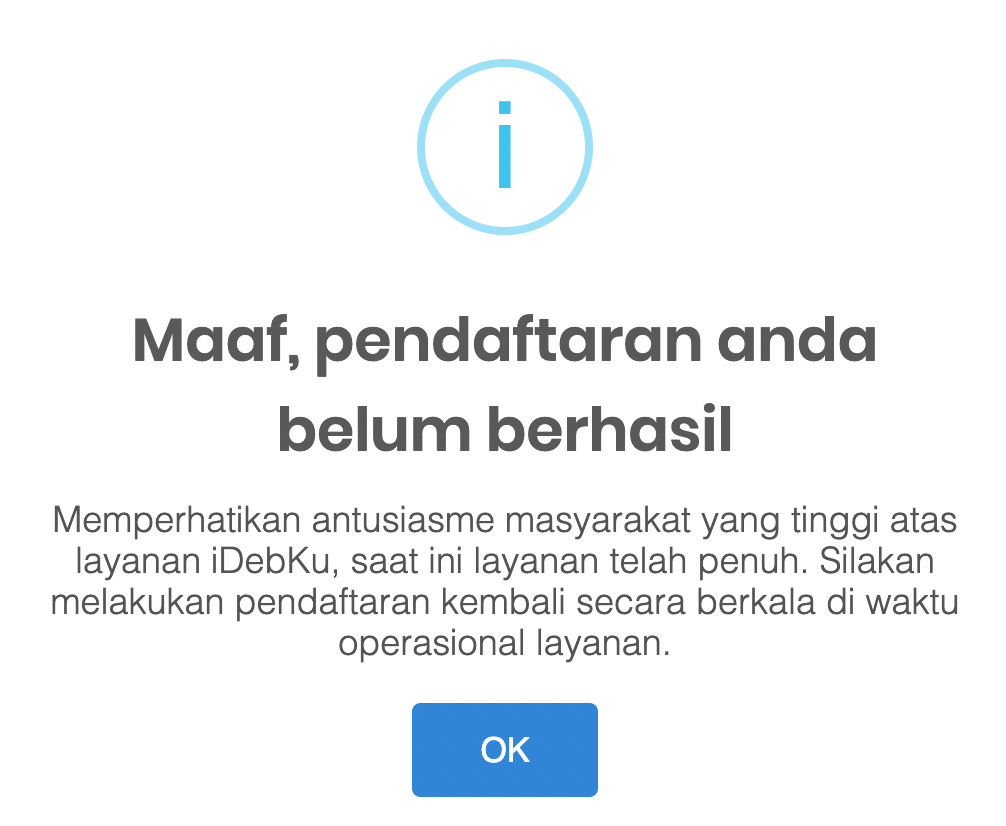

The alternative route to get one’s credit report is through SLIK’s system itself — provided by OJK (the financial services authority of Indonesia). Consumers can either go physically to a branch, or enter a web-based portal called Idebku to get their free credit report. The only issue is that accessing the portal requires one to compete against an extremely limited daily quota, and most people who attempt to check their credit report are unable to, getting hit by an error screen during entry:

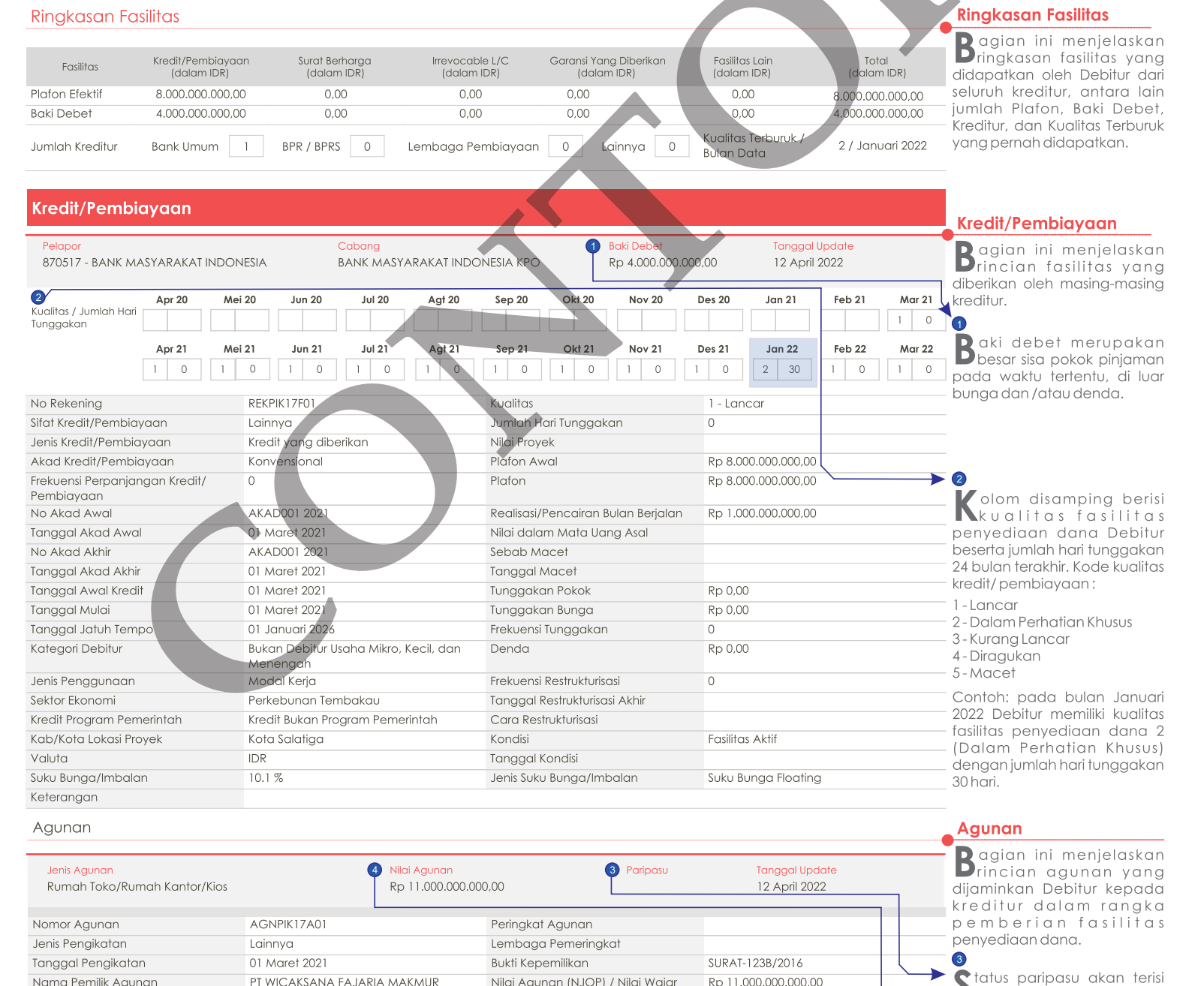

And even if users are able to get their credit report data, it’s presented in manner that’s not entirely easily understandable to the everyday consumer (given the main audience is supposed to be a bank analyst). Here’s an example of the report one would get from OJK’s Idebku portal:

There are a few “innovative credit scoring” fintech players that aim to recreate the credit report with alternative data sources (e.g. e-commerce data, P2P data, customer-permissioned data). These players include Cekaja.com, Finantier, and Koinworks. However, these are unofficial lending data aggregators, and thus the credit score they provide is largely not representative of what formal credit providers actually “see” when assessing a customer’s creditworthiness (given that they do not have access towards the customer’ credit report unless they are lending customers).

II. Furnishing mechanics — what if information goes wrong?

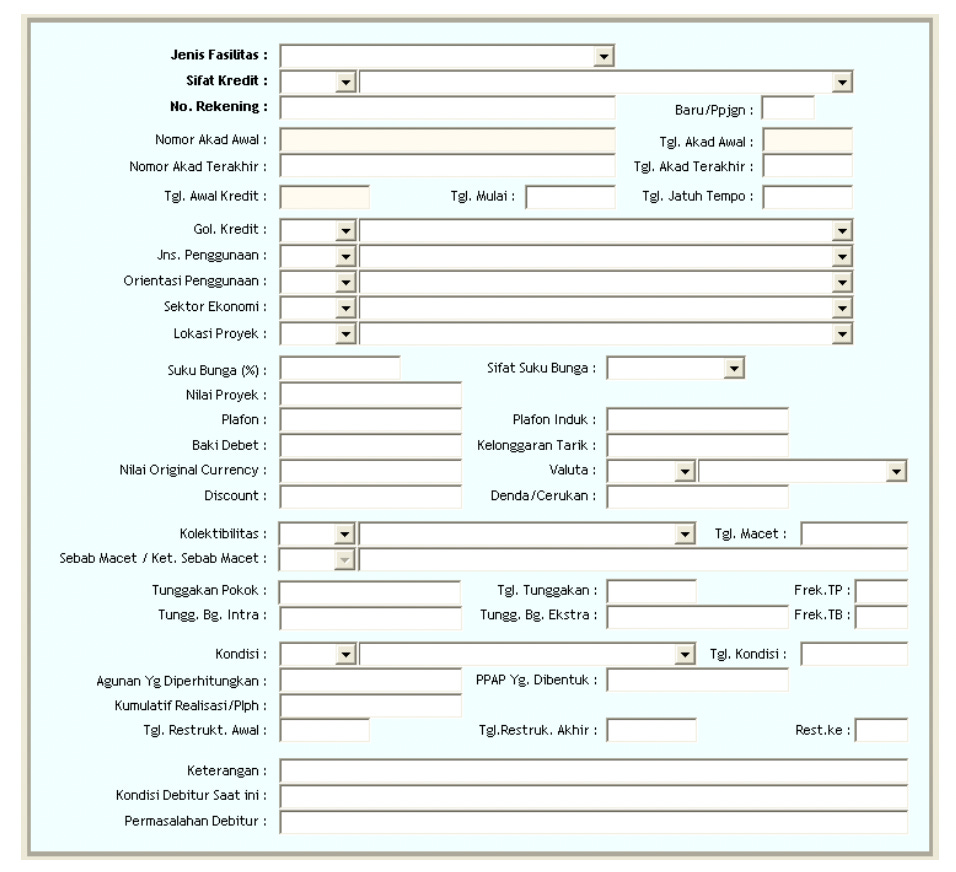

Rules around furnishing govern the entry of all new data into the credit reporting ecosystem. Data is typically reported monthly and includes dozens of fields (e.g., customer name, customer address, credit limit [if applicable], current balance, account status, etc.). Below is a sample of what furnishing credit data entails:

The complexity of the furnishing process—dozens of fields to fill in, with a wide range of possible values for some of them—means that furnishers occasionally must make judgment calls, and errors can oftentimes happen. A non-exhaustive list of potential problems includes:

Corrupted/incorrectly entered data: suppose an auto loan is accidentally entered as a personal loan, or a consumer’s successful monthly payment is erroneously recorded as late. Either of these errors will cause the credit file to be partly incorrect, which means that the (1) customer’s credit standing might be rated differently, and (2) the credit file reported to the lender will also be inaccurate — thus having a bad impact on underwriting decisions. Ironically, a VC who we were speaking found a late credit (that was not supposed to be marked as late) on his credit report — so this can happen to anybody.

Consumer identification or matching errors: SLIK must correctly match the tens of millions of credit line datapoints that they receive each month to consumers. If two credit lines that belong to the same consumer are not both matched with that consumer, then the consumer will end up with an incomplete credit report.

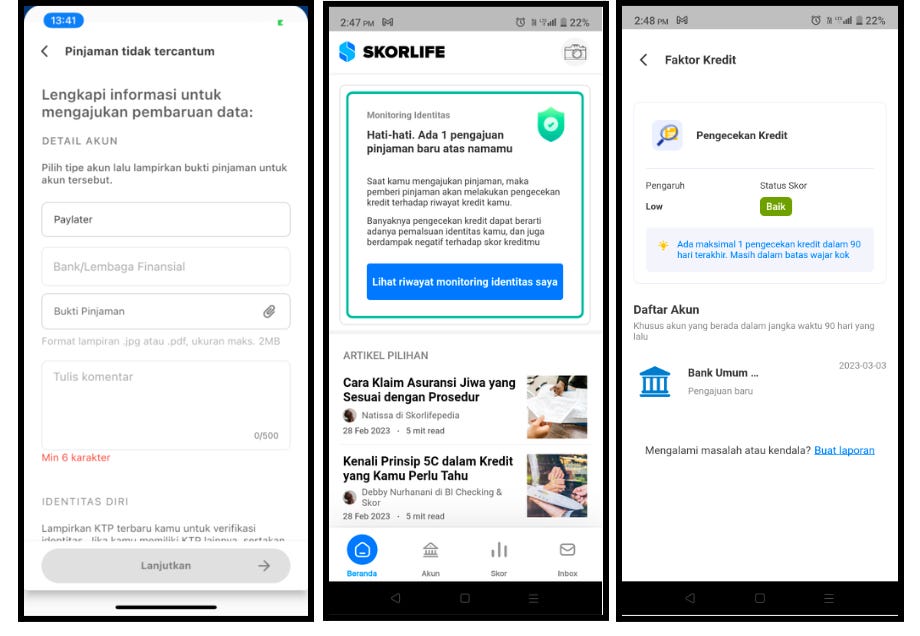

Identity fraud: credit products issued to individuals with fabricated identities are not unheard of. Fraudsters piece together names, social security numbers, and other identifying information to create identities. Many of Skorlife’s users have had issue when they’ve checked their credit report and noticed that there are loans they have never applied for, that show up in their credit report.

Given the likelihood of wrong data entering the system, there needs to be a process that ensures that users can have “control” over their data and have the ability to dispute. However, the lack of credit literacy and access for people to check their credit report have made the ability to dispute very difficult. In one of the credit bureaus I engaged with, they mentioned that “nearly zero” consumers have directly disputed their credit information with the bureau itself. If you’re not aware of the fraud itself, you don’t even know that you have to address it.

However, doing so is actually relatively straightforward, and there is a regulatory clause (SEOJK 2014/7) that mandates that financial institutions must address customer complaints that have the potential for financial losses in under 20 days, with an additional 20 days for resolution. OJK itself provides a direct stream to the financial institutions to report any wrong information (including credit disputes) in a portal called APPK (or Aplikasi Portal Perlindungan Konsumen).

The takeaway is that the necessary infrastructure and regulations actually are set in place for consumers to take fair action over their credit standing and protect their reputation. The major issue is that most are not even aware (until potentially too late e.g. at a point where they do need credit and are rejected) of their data, and hence have a lack of ability to take proactive control.

III. The implications to low credit literacy in Indonesia today

With low financial literacy rates, difficult access to credit standing data, coupled with the low formal credit penetration in Indonesia — it’s unsurprising that credit literacy is extremely low in Indonesia.

However, low credit literacy and low formal credit penetration do not imply low credit demand. According to the Indonesian credit bureaus, there are ~70 million people in Indonesia who have credit records. Out of these, it’s estimated that >20 million are those who have taken Paylater loans (assuming Kredivo has ~10 million users and ~50% BNPL market share), which are recorded in the credit bureau. From quick analysis, Paylater users in Indonesia are largely “unique”, tending to have the Paylater as their only form of credit. This is due to the fact that Paylater loans tend to have been disbursed in a “volume-based” manner, with less stringent underwriting than formal financial institutions like banks — hence unlocking a set of users that potentially could not be served in the past by formal credit. This implies a few things:

Formal credit penetration (beyond just credit cards) is low: probably below 50 million people in Indonesia: implying a 20-25% penetration rate;

Credit demand is high: BNPL has only existed since about 2016 in Indonesia with a huge growth spurt in the COVID-period. In the span of 5-7 years, assuming that Paylater users largely only have Paylater — it has grown to 25-30% of the credit bureau population.

The dynamics between low credit literacy, low formal credit penetration due to banks' low risk tolerance and high credit demand can be dangerous — especially in a country where credit access becomes easier and easier to obtain, largely due to expanded digital channels, >70% smartphone penetration rate, and the loan-book growth of volume-based lending fintechs & P2Ps in the region. There are a few concerns that I have on the lending landscape generally, and have seen personally through stories from Skorlife's users:

Customer acquisition for new-to-credit customers begins through "easy" access to unsecured online loans which hurts them in the long-term: college students or early professionals are first exposed to credit through Paylater or online loans. These channels offer seamless access to credit, but can easily be mismanaged due to their short tenors and high interest rates. One user I spoke to managed >5 online loan applications, first for “productive purposes” (their business), but the ease of obtaining credit quickly and oftentimes with promotions led the user down a path of overextension — taking on more and more loans and transitioning to becoming a highly consumptive user of credit (for shopping, big-ticket items).

Increasing reliance on online loans as a "loan of last resort": if one mismanaged credit in the past (willingly or unwillingly), or had an incident where they damaged their credit history in some way and did not fix it -- banks likely would not lend to them. A user I spoke to mentioned that they lost their job in the midst of having two installment-based loans (including a mortgage). The sudden loss of a stable income meant that the user had to pay late for a period of time, prioritizing their direct expenses and obligations first. When looking to take on financing to open his business, the user could not get access to a bank loan. The easiest alternative was to get online loans, which for the reasons above ended up resulting in mismanagement, ballooning debt, and the incessant chasing of debt collectors who resorted to harassment to try to get the user to pay back.

Not proactively thinking about one’s credit standing until it’s too late, hindering one from opportunities to further one’s life: As mentioned in the section above, it’s not rare for incorrect or even fraudulent data to appear in one’s credit report. However, if one does not proactively check one’s credit report, these errors could only pop up when one applies for credit (and realizes their credit standing e.g. when they get rejected). One of our users, for instance, found a defaulted loan in their credit report that was not even theirs when applying for a car loan and got rejected, hence not being able to follow through with what was supposed to be a very meaningful purchase for them.

It's fantastic that the credit access problem is being solved by fintechs today. As I've always believed: credit is an enabler of opportunity when used right. However, the latter part of this sentence ("used right") largely has not happened today in Indonesia at scale. Part of the reason is that general financial literacy is low and hence credit education itself likely is not well spread, but another part of the reason is that access to one's credit data itself is very difficult to obtain (which prevents them from thus proactively protecting, managing, and improving their credit standing) despite the infrastructure for credit data and protection being in place.

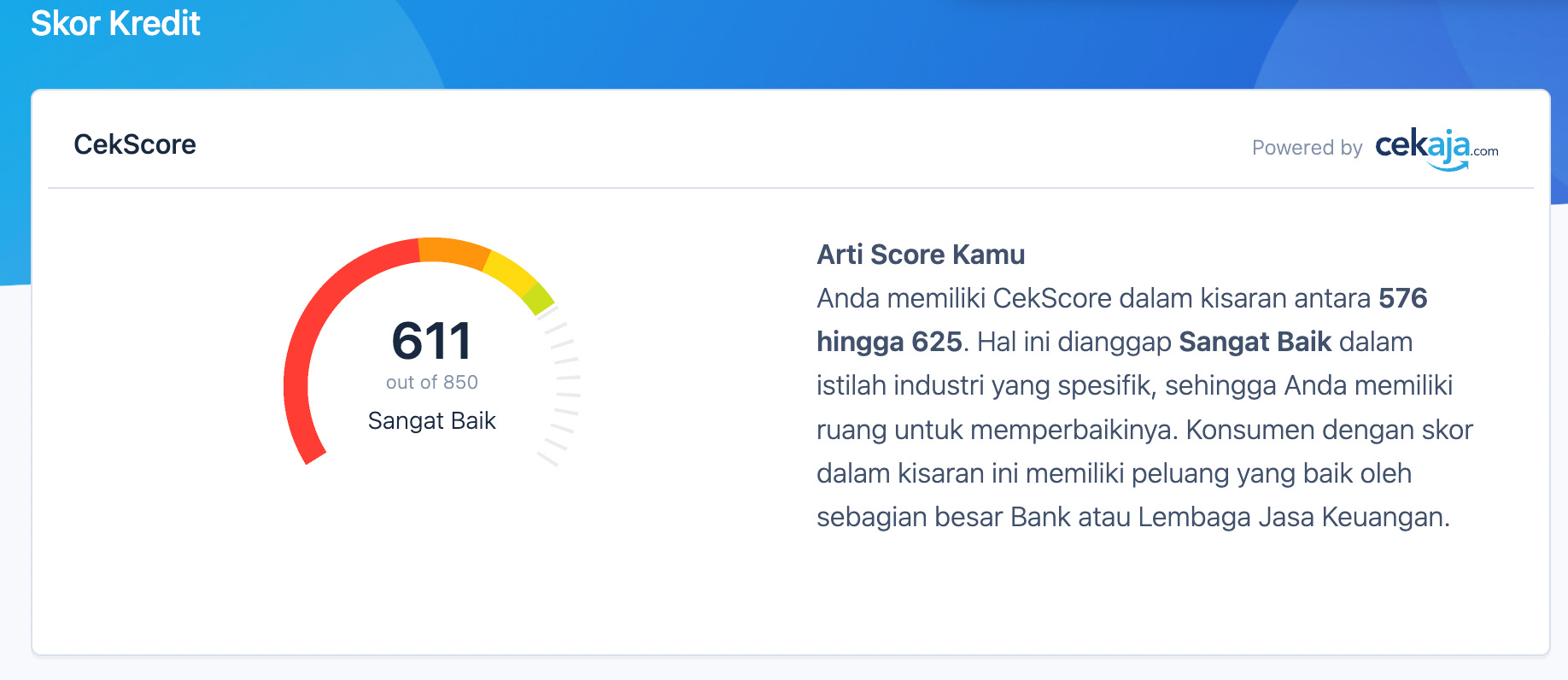

I believe that this is one of the most important problems in Indonesia today, and is the mission that I’m undertaking now at Skorlife.

IV. Building consumer access to credit standing data to build literacy

Let’s bring back the mind-map of the credit data space in Indonesia again.

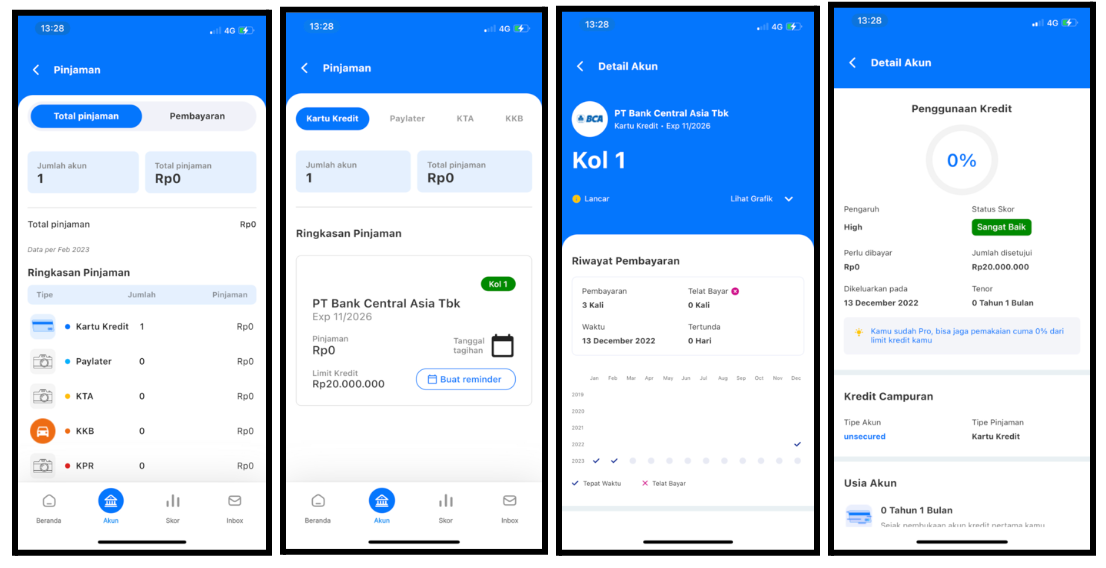

The company I’m part of building, Skorlife, aims to sit as a consumer-centric amplifier to the already existing credit data infrastructure by partnering with an already existing credit bureau, and serving as their acquisition channel to serve B2C users. We know that the largest pain point for consumers in this space is accessing and understanding their formal credit data — and so Skorlife provides a seamless, secure, mobile-first, and educator-centric way for customers to get a full view of this data in less than five minutes after a comprehensive KYC process.

It’s important to note that Skorlife is not a credit bureau (LPIP) itself, and actually is recorded as a financial planner financial technology company (IKD) under OJK’s regulatory sandbox. When serving consumers in such a space, data security and customer’s consent are extremely vital, and hence they are Skorlife’s most important pillars. We implement a stringent KYC process through a registered electronic certification provider (PSrE) VIDA, have optimized for security in all aspects (having received the ISO-27001 and 27701 certifications), and Skorlife’s data flow requires that users directly consent to their credit report being sent to Skorlife (and if not consented, that users have full access of their credit report sent by the bureau via e-mail regardless). Although we are a fintech, we can’t “move fast and break things”. This space requires you to be methodical and think of the customer’s safety and benefit from all potential edge cases and angles.

Why don’t do the bureaus directly focus on a consumer play when they already have all the data and assessments in their hand? The short answer is they can (and do — e.g. Pefindo’s B2C business), but bureaus largely don’t focus on their B2C business today because building the engineering and operational capabilities to run a scaled consumer business is challenging and entirely different than their B2B side (which is largely where they make money today). As Steve Jobs said: “The only dangerous competitors are focused ones. Focus is about saying no.” Another way to put it is that business strategy is about trade-offs. Without trade-offs, there would be no need for choice and thus no need for strategy. Skorlife is committed to fully focusing on helping consumers access, understand, protect, and improve their credit standing. That’s why we work with a credit bureau to help them build a B2C business without sacrificing their focus from the B2B side they should be focusing on.

Skorlife’s mission is to broaden access and amplify credit literacy in Indonesia at scale. While we provide access to the credit report data, the most important thing in a consumer business is to solve the customer’s jobs to be done in the deepest possible way. For instance, beyond just giving access to a stream of data, we give the user personalized advice to understand how to improve their credit standing (through our own internal insights engine). This enables users to understand how to take their next step (for a particular user in debt across multiple loans for example, the knowledge to prioritize which loan they should pay first).

And we also protect. As mentioned before, incorrect data can surface from multiple places due to the complexity of the credit furnishing process. By providing users access to their credit report data, we also have the ability to help users complete the next leg of their journey which is to dispute any incorrect data, and to monitor their identity being used in any credit application.

There’s a lot of work to do, and the goal to building credit literacy in Indonesia will not be easy given its low financial literacy rates today. As someone who has been in the formal education space for multiple years (teaching in the Chicago Public Schools while I was in college, doing an internship with Teach for America, building an education non-profit in the college acceptance and job mentorship space, and working in the Indonesian Ministry of Education) — I realize that the mission to further credit literacy to the next 100 million Indonesians requires more than just “building an app”.

There’s a responsibility that Skorlife has to do all the work it takes to further credit literacy and education beyond just product. It’ll take working hand-in-hand with the regulators. It’ll take building partnerships across companies, schools, and communities. It’ll take really focusing on building the mindset of an educator, as a company that loves and genuinely wants the best for the lives of the people we serve, to help us to fulfill our mission.

On a personal note, that’s why I’m here today stating my deep commitment towards this mission. Skorlife plays an important role in the credit data infrastructure space especially in bridging a complex topic to the mass.

Conclusion

As we saw in the beginning, Credit Karma today currently has 120 million users in the United States alone. Its use has been correlated with users increasing their financial well-being and their ability to pay back their debt. The “Credit Karma” effect goes beyond just building a great business — it’s an infrastructure that has helped millions of people be able to better manage their credit standing and hence open up opportunities, or at least protect them from mismanagement.

In Indonesia, we see that the credit data infrastructure is nascent but decently robust. Unlike other countries, there is a centralized debtor database managed by the national financial authority OJK. There exist a suite of credit bureaus in the market who are helping further the understanding of customer’s creditworthiness through additional data sources and analytics. There are also regulations set in place to help consumers directly with protecting and disputing their data.

However, because consumers do not have readily available channels to access their credit data and the tools and educators to help them understand it (coupled with low financial literacy), there is not really any proactive “push” today in Indonesia to educate users that having control over their credit standing data is an important part of their life. The biggest issue is that lack of understanding of credit data — coupled with even easier access to loans through channels like BNPL or P2P — means that the dangers and likelihood of mismanagement are higher. After all, how are you to know as a new-to-credit college graduate that paying back your Paylater loan “a couple days” late would be so detrimental? There’s a lot of work to do, and Skorlife aims to solve this problem by augmenting access and understanding to credit data. Hopefully for the next 100 million people in Indonesia, like Credit Karma has done.

Bringing the back the question: “Do you know your credit score?”. It’s very likely that you don’t. But now that you’ve made it to the end — I encourage you to go check it out, take control over your credit data, and take ownership over your future.