A first principles deep-dive into FinTech for operators (with a focus on Indonesia) - Part 1: Lending, Neobanks, PFM, and Infrastructure

An in-depth guide to FinTech designed for operators and entrepreneurs to not just develop cursory understanding, but deep-enough first principles to get started with innovating in the space.

Welcome to part one of our series on the FinTech industry:

Part 1: Lending/financing, consumer banking, PFM, infrastructure ← This post

Part 2: Wealth/investments, business banking, payments, insurance (coming soon)

Entering the FinTech space for the first time as an operator is an overwhelming step, regardless of which country you reside in. Complex terminologies abound, and it feels almost impossible to learn everything especially given the breadth of the space (lending, wealth, PFM, etc.). However, it has become tremendously vital for operators to be attuned to the broad space regardless of which vertical you currently operate in. Firstly, because finance is literally everywhere. Embedded finance requires operators in every field whether it’s commerce or SaaS to understand FinTech as a key lever for monetization. This could be benefiting users (e.g. Paylater products offered in e-commerce), or benefiting key agents in one’s value chain (e.g. for ride-hailing, enabling drivers to get access to financial products / earned-wage access).

Second is due to the fact that we’re entering a time in the FinTech industry where the concept of “rebundling” (or companies going multi-product vs. just focusing on a single core point solution) is much more possible with available infrastructure (e.g. vendors for KYC) and a higher density of trained FinTech talent. As Rex Salisbury from Cambrian Ventures states: rebundling by very definition captures larger markets, results in stronger business models due to synergies (cost, data, etc.), and creates a better product experience from product connectivity (especially with captured user data and ability to use AI to create further user impact). We already see this happening now in more established markets, with a few examples:

SoFi building a Credit Karma competitor called Relay (growing 90% YoY), as a lead-generation tool for their lending business

Nubank acquiring banking licenses across their key markets (most recently announced in Mexico) to facilitate product expansion and cheaper cost of funds for their main credit card business;

Even attaching fintech and non-fintech together, with fintech companies realizing that SaaS or e-commerce revenue can result in significant add-ons (e.g. Klarna with their AI-powered shopping feed, Toast using SaaS as their initial wedge to offer financial products to restaurants, and Jeffrey Bussgang’s flipped-playbook thesis on offering financial products first before vertical SaaS).

Even if one works in a single FinTech “vertical”, you’d still have to build knowledge across these dimensions. If you’re in lending (e.g. building a Paylater product), you’d have to connect to a payment gateway, manage take-rates across products and merchants, and leverage alternative data sources from infrastructure providers among other vendors. Having an understanding of the industry allows one to be better prepared to tackle the broad challenges of the incredibly fast-growing space .

In this article, I’ll go deep enough to give one a sense of the broad areas of FinTech, segment the space to cover the various sub-areas one can tackle in the space (e.g. in retail lending — one can focus on subprime lending for those in T2/T3+ cities), and operating considerations and strengths one has to develop to “win” in the space. I’ll tackle this from a perspective not just useful to develop cursory understanding as an investor, but to actual develop first principles useful as an operator. I hope that this can benefit those new to the FinTech space in Indonesia and even beyond. Let’s start our journey with business models focused on lending and financing.

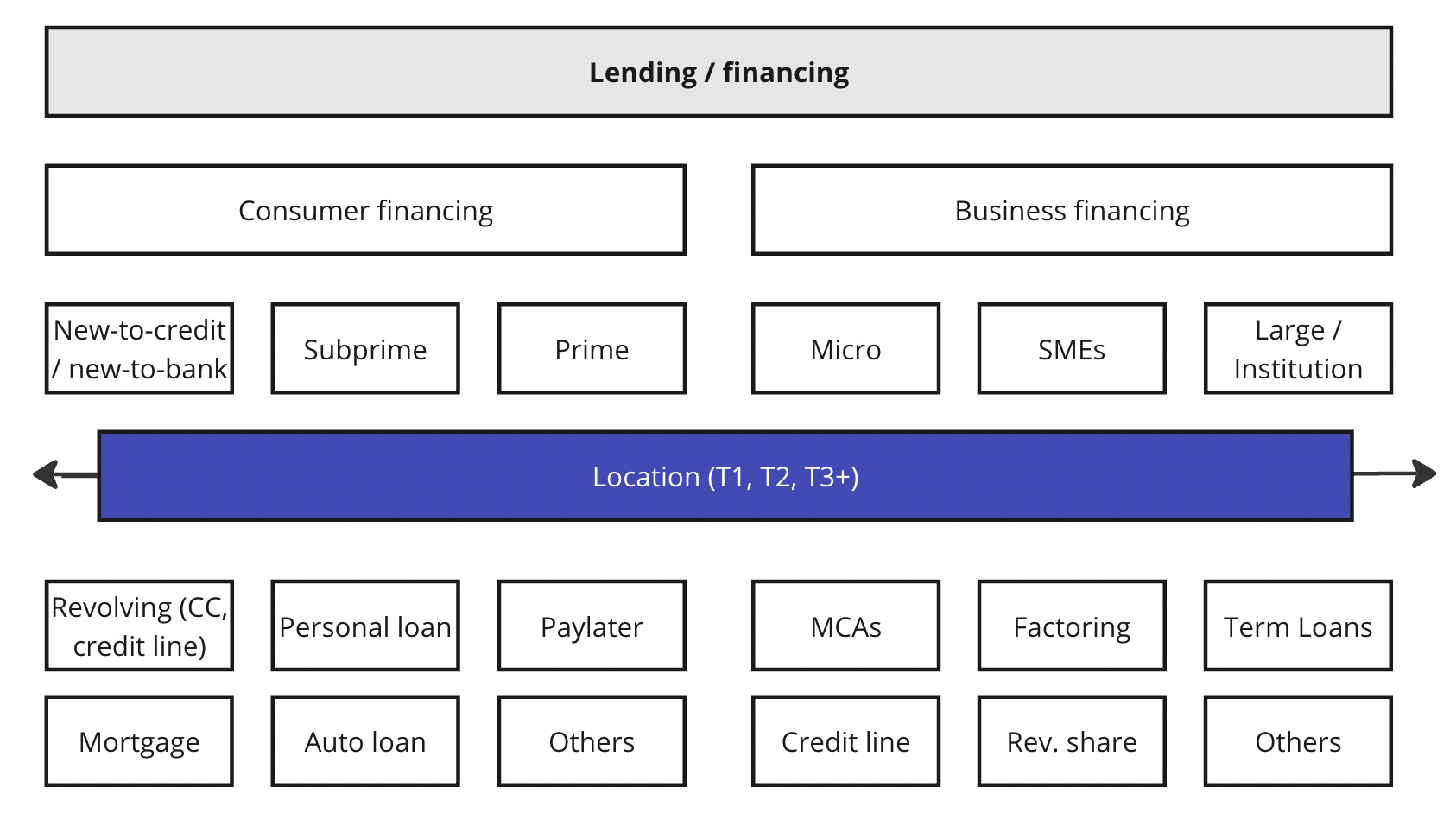

Lending & Financing

The above graph is obviously an overly simplistic picture of the lending & financing space, but captures a good-enough depiction of how to think about it (one can further segment — e.g. for business financing, into types of businesses; for consumer financing, into income types). The most direct split is at the top, between financing for consumers and businesses. Let’s begin!

Consumer financing

For consumer financing, the table below captures how I think in broad strokes about segmenting needs (emphasizing that this is broad — this could also differ based on product type; for instance, credit cards for sub-prime in T1 are still under-penetrated despite Paylater and online personal loan product penetration growing).

Credit penetration has increased quite significantly over the past few years in Indonesia, with ~80 million people with records in the credit bureaus (for more on that, check out my article on the Indonesian credit system here) — which is around a 40% penetration rate amongst working adults (growing from around 20-25% penetration just 5-7 years back). Credit is growing in terms of access in Indonesia at a rapid pace, fueled by digital financial services (which is estimated to grow by~25% a year to a $15B loan book by 2025 according to Bain’s SEA 2023 e-Conomy report):. However, credit penetration highly differs amongst product types: for instance, credit card penetration sits at roughly 4%.

Below we’ll tackle how tackling each user risk segment requires distinct approaches:

Prime

Prime customers have generally been the main customers of banks in Indonesia. Banks have scaled throughout the archipelago with bank branches even in most rural areas, but for financing find it difficult to lend to those who are non-prime and in areas where they don’t have field collections infrastructure (generally in T3+ cities).

Given that prime customers generally do not have an issue accessing credit, the main challenge lies in optimizing the credit experience. This could be anything from price (lower interest rates), rewards (e.g. higher multiples on credit cards for premium items: Krisflyer), user experience (e.g. for credit cards, digital onboarding & design), seamless integration with other financial products like one’s bank, or brand (e.g. BCA immediately having the view of being “high-class”). Companies focusing on this space need to focus on having a 10x experience on one, or a few of these pillars. For instance, Yonder, a lifestyle credit card company in the UK, rewards customers for purchases for points specifically redeemable for food, beverages, and entertainment.

In addition, credit cards are a category of loan products that is still under-penetrated amongst the prime (as mentioned, only ~8 million people are estimated to have cards, which is only about 4% of the population). This is also due to the fact that credit card interchange fees (or “MDR”) are much higher, resulting in many merchants not accepting credit card as payments especially outside of T1 cities. Challengers like Honest Bank and Xendit are attempting to fill in the gap with credit card offerings of their own pushing differentiation in the form of rewards, digital onboarding, spend analytics, reminders — essentially a better experience overall.

The right-to-win in prime comes down to distribution and creating differentiated user experience. One cannot think of themselves as simply a “consumer lending company” but rather a company obsessed about creating a world-class brand with absolute product joy (think Apple with their Apple Card).

There are also players like Cermati or Ringkas who act as aggregators for loan products generally focused on prime customers (everything from personal loans, credit cards, mortgages). However, these tend not to be lenders themselves and their business models lie on referral fees meaning that distribution is everything. We won’t focus on these aggregator-business models too much.

Subprime

Sub-prime customers have generally been the main customers of fintechs and multi-finance companies in Indonesia. With their strength in underwriting (due to stronger data capabilities) and without as many regulatory constraints as banks, fintechs are able to lend to more risky customers with the caveat of higher pricing (currently fintechs in Indonesia are able to charge 0.4% interest per day, which is being regulated down to 0.3% starting from 2024). We can see an example of risk-based pricing from Honest Bank’s credit card, which elevates transaction fees for sub-prime users up to RP. 150K per month or $10 (this is high!) given that credit cards have an APR cap of 21% in Indonesia.

There are ways to circumvent regulations to either move faster or to enable higher pricing (imagine having a single revolving credit line and splitting it into multiple prepaid cards — circumventing the necessity of getting a credit card issuing license and the APR cap), but this is generally not recommended given the gray areas involved. We know that FinTech regulations are strict, and we saw in other countries how regulators could turn-off the tap so to speak at a whim (RBI shutting off credit card companies Uni and Slice by banning credit-line backed prepaid cards).

Non-fintech players have also managed to bridge fairer financing access into the subprime space through innovative models. Pegadaian, a state-owned enterprise, offers a pawnbroking service (generally against gold, but could also be jewellery, motor vehicles, etc.) that unlocks 120-day credit for 0.75-1% interest accumulating per 15-days. With administrative fees, this could easily get expensive. Multi-finance companies with physical strongholds in T2/T3+ cities that enable them to do collection are also able to bridge to sub-prime (again with higher interest rates).

Risk profiles are correlated with income, although obviously not fully (there are poor prime-customers, and rich sub-prime customers) which makes sense given that ability to pay is one of the characteristics that predicts whether one would default or not. For poorer customers, one differentiating characteristic is the certainty they need on loan approval. Getting rejected for financing is a dejecting feeling (one most of us reading this would probably never understand). That’s why these customers are willing to make the trade-off of higher pricing for the certainty that they get in return. You can see this fervor from the sub-prime’s active daily participation in Facebook communities to help them with stronger certainty on credit approval, as shown below.

Companies focusing on sub-prime can win if they can differentiate on risk-based pricing (e.g. through better underwriting) or who can unlock new ways of preventing downside risk (e.g. like Pegadaian, collateralizing valuable items, or BRI Finance having field collections operations across many T2 cities). Advance Intelligence Group is an example of a FinTech behemoth in Southeast Asia that exhibits this: having majority ownership over a licensed credit bureau in Indonesia called Credit Bureau Indonesia. Owning this data infrastructure likely enables them to train underwriting models on the ~100 million bureau records in Indonesia — which powers their ability to outcompete in their subprime lending businesses.

Collections is a key function that sub-prime lenders need to focus if they even imagine to get a certain level of scale. Kredivo purportedly has a team of 1,000+ collections agents (both desk and field), and Indodana works with 10+ outsourced agencies. Having boots-on-the-ground and differentiation in reach can make a big difference. Amartha for example has run profitably for the past four years due to very strong collections capabilities through community partners in rural areas.

Here are a few examples of standout sub-prime focused businesses abroad:

Yendo (securing $23M Series A this year), a FinTech company in the US, innovated on collateralization by enabling the subprime to obtain a credit card by backing it with their car. We see multi-finance companies already do this successfully, although with remarkably high-interest rates. There is likely still room to play in this space.

Capital One pioneered this focus on doubling-down on subprime lending in the United States. Serving subprime customers requires careful attention to underwriting, economic cycles and data. If you’re good at consumer credit, you can have outsized returns. If you’re bad at it, you can blow up. Building graduation schemas also enables customers to “prove themselves” over time by gradually providing them higher ticket-size loans or limits. This effort is incredibly analytics-intensive and experimental. The right to win lies in a team that can execute on this type of skillset.

New-to-credit / new-to-bank

New-to-credit and new-to-bank customers are generally the most underserved due to the difficulty of accessing their creditworthiness. However, they comprise a large portion of Indonesian working adults (roughly 60%). Alternative data sources (e.g. e-commerce, cash-flow, telco data) are required to assess their creditworthiness with players like Tokoscore offering this — but it’s still quite difficult given that these data sources don’t truly predict one’s creditworthiness.

The P2P association in Indonesia (AFPI) also has a real-time debtor database that one can utilize to assess creditworthiness of these customers. However, this database today is only accessible to other P2P players. Hence, gaining access to formal credit for new-to-credit or thin-file customers is still difficult. OJK has stated their intention to enable the credit bureaus to access fintech borrowing data, which once completed at the end of 2023 would help these users with fairer access to formal credit.

In the United States, products like credit builders have gained strong traction — helping the new-to-credit build their creditworthiness through regular payments. Capital One also pioneered the concept of a secured credit card, where customers with little to no credit could pay, for example, $1,000 as security (potentially in a fixed deposit or savings product) in exchange for a $1,000 credit line and begin building a progressively larger line by paying on time.

However, in Indonesia these credit builder products or even secured credit card products are pretty much non-existent (the only one I could find was by Sinarmas, and going through the application process was a massive hassle taking more than a week). And perhaps rightly so, as the concept of “building credit” itself in Indonesia is not as intuitive as in the United States (where there’s a unified FICO credit score and people generally know the implications of different tiers of scores). In Indonesia, as I explained in my article, the different bureaus have their own methodologies and access to consumer credit reports has been a challenge until recently.

Moreover, building a credit builder product as a startup is difficult as the economics are geared on customer lifetime value rather than immediate payback given the fact that interchange revenue is likely very small and net income including acquisition costs could even be negative (as explained by this report by the Center for Financial Services Innovation). If a lending company is able to crack a multi-product scheme with credit building in mind — there could potentially be a strong retention moat (although also bears risk, as these customers can also switch to other products).

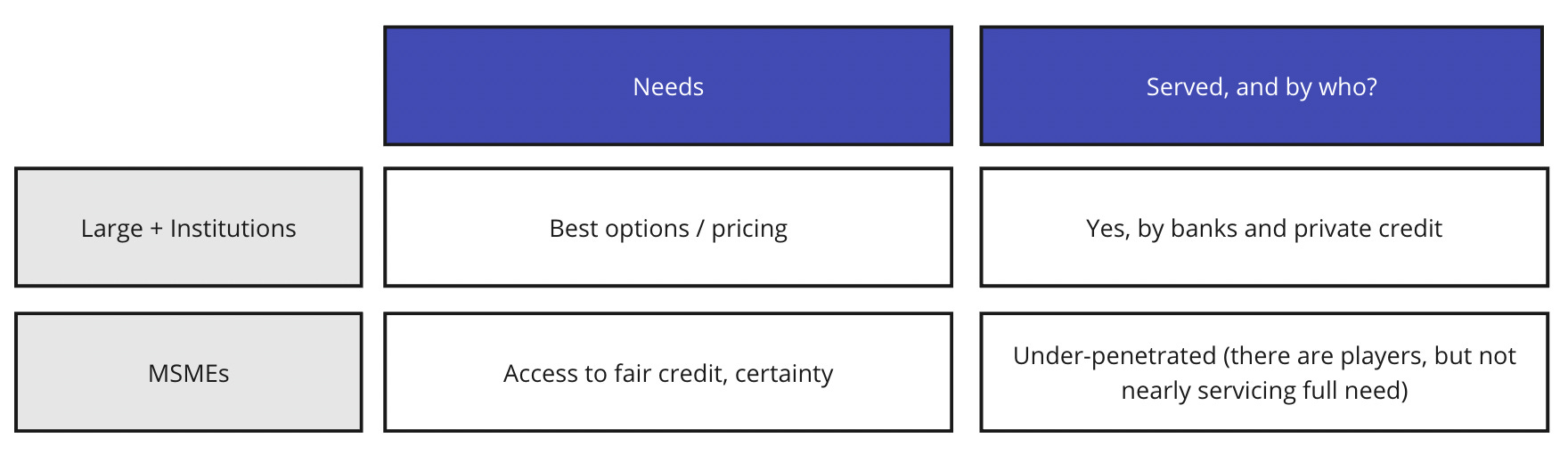

Business financing

The FinTech game in business financing is to service the 60+ million SMEs in Indonesia (likely not even including the micro-businesses like cooperatives). Large enterprises are already very well-served by banks and private credit, which have traditionally not placed their focus on MSME lending. We’ll focus our attention on where MSME lending is placed in Indonesia, and similar to consumer financing build up a vision of where it will be placed and how one can “win”. If one wants to read a great book on this sector to develop a strong-enough framework of understanding, I recommend picking up FinTech, Small Business, and the American Dream by Karen Mills.

MSME Lending

The difficulty of small business lending

There are three main difficulties with MSME lending and why banks have traditionally found it difficult to service this segment for financing.

Information opacity: Reliable information on small businesses are difficult to obtain because the operating performance, financials, and growth prospects are difficult to see and predict. Little to no public information is available (even in the bureaus), and most MSMEs are run by inexperienced or busy owners who may lack detailed balance sheets and income statements. This makes it more difficult to tell creditworthy or non-creditworthy businesses apart, and to also conduct verification on these businesses to separate out bad actors.

Heterogeneity: All businesses are different. A “good” HVAC company will be very different from a “good” dermatology provider, which will be very different from a “good” biotech startup (from a margin and operating structure perspective). Unlike consumer financing, it is harder to generate a “truth file” — a formula enabling a lender to understand whether one is creditworthy or not. It requires one to deeply understand the operations of a small business (either specializing in an industry, or spending a lot of manual work and time to do so) or to minimize risk, require collateral (which most small business owners might not have or want to go through hassle to process).

Economics: It is structurally more profitable to do loans to larger businesses, given the opportunity costs of more difficult underwriting as described above coupled with the smaller-ticket sizes of the loans itself. To top it off, secondary markets for small business loans is not robust meaning that it is hard to off-board or manage the loan portfolio itself. If one wants to create a profitable small business lending company, one has to be able to scale — which as pointed out above is difficult due to the problems of opacity and heterogeneity.

Given these facets, small business lending has not really scaled too strongly in Indonesia. According to OJK, the MSME loan book as a percentage of their contribution to GDP in Indonesia is around 14% in 2022. This is much lower than other countries’ in Asia-Pacific: Thailand is highest at ~80%, Singapore at ~40%, and India at ~25%. According to Koinworks, only ~30% of the country’s MSME’s are getting access to financial products. There is clearly much more room to grow in terms of growing credit penetration for the country’s 60+ million MSME’s. We’ll dig into how below.

Types of small businesses

As mentioned above, small businesses come in different shapes and sizes. It’s important to understand these various types as their needs differ greatly (e.g. businesses requiring growth capital are different than those requiring loans to protect against operating expenses in the midst of seasonality). In general we can think of small businesses in this framework (as depicted above):

Non-employer small businesses are sole proprietorships without paid employees (contractors, freelancers, ride-share drivers, painters, agents, etc.). Innovation has grown this type of small businesses a lot, promoting roles in the “gig economy”.

Main street firms are local restaurants, gift shops, car repair operations, and other storefronts we imagine when we think of a small business. An increasing number of these small businesses now leverage the Internet to ship goods outside of their regions, but most still reside or function mostly locally;

Supply chain firms are small businesses that supply large firms and governments (e.g. trucking and logistical services to companies like Coca-Cola).

High-growth firms are businesses like technology startups or high-growth brick-and-mortar businesses (such as F&B chain expanding to hundreds of locations, good example of this is Champ Restaurant Group in Indonesia)

We can further segment these types of businesses into different industries (whether it’s F&B, import/exports, manufacturing, or even mom & pop stores selling on e-commerce channels), or geography. The point is that it’s vital to understand the type of business and their needs before deciding on the financing product that best fits them (based on term length, quantum, etc.) and also on how to conduct underwriting for them. We’ll dig into this below.

Types of financing options

There are many different types of financing options available for small businesses, and especially with owners who do not have the full understanding — getting the business-product fit that makes sense is difficult if one does not have a direct relationship with a banker the same way a larger enterprise does.

Generally speaking, there are a few types of financing options available to small businesses looking for non-equity loans:

Term loans: Paid back on a set schedule — often used by small businesses to buy equipment or real estate — more expensive and longer-term;

Bank lines of credit: liquidity available for business to draw down on immediate basis to smooth out uneven cash flows — tend to be lower-limit;

Merchant cash advances (MCAs): let businesses get lump cash advance; the lender is repaid by taking a percentage of businesses’ future sales in short-term;

Receivables financing: pledge some of businesses’ accounts receivables to a third party. In return, it gets immediate cash in an amount which represents a discount of the total receivable (compensates third party for taking on risk that it cannot collect full amount of receivable) — very specific towards AR use case;

Business credit cards: tend to be most accessible, but also expensive (carrying high interest rates, also generally lower limit)

One challenge for FinTech is to facilitate business-product fit: MSME lenders who can guide businesses to select the financing option that best fits their needs (whether in terms of quantum, or term-length, with the requisite dollars owed when one is to accumulate interest alongside the principal). Holistic MSME lenders like Koinworks and Investree do this well: having a wide spectrum of products designated for particular MSMEs and easily-reachable service touch-points to help guide businesses.

The other potential innovation touch-point is to actually create new loan vehicles that may not have existed for small businesses. Bonside, a brick-and-mortar small business financing company in the United States, pioneered the Repeatable Revenue Agreement (RRA) which provides growth capital in exchange for a share of monthly revenue up to a previously agreed upon multiple (the business can fulfill this as short or as long as it takes — but usually planned to take 4-5 years based on projections). This loan vehicle is less expensive than a term loan, large enough to finance expansion needs without sacrificing equity, and gives the business enough time to payback without hindering operations (unlike potentially an MCA). However, this type of structure is only possible because the business specifically focuses on a niche (brick & mortar) for a specific type of financing need (growth capital, specifically to open up new branches) — allowing for greater predictability in forecasting. There is a startup in Indonesia currently in stealth working to build this model out starting with F&B businesses, so I’m excited to see this start to pan out in this region.

Innovation in MSME lending and potential opportunities

Generally speaking small business lending had to overcome two structural gaps in order to be performed effectively: ease of customer experience (including onboarding) and visibility of small business finances to lenders for underwriting.

These structural gaps were tackled through digital onboarding (small business lenders streamlining steps of application), the rise of e-commerce and the availability of data that it finally presented. Koinworks (who serves 1M+ small businesses today) funded online merchants exclusively in its first year due to the availability of verifiable data that existed (e.g. on Shopee or Tokopedia) for them as opposed to non-online merchants. As credit bureaus came into the picture with available API infrastructure, this ecosystem enabled small businesses to be underwritten and serviced much quicker than before (in minutes vs. days/weeks). This is why we see e-commerce companies like GoTo or Shopee offer its own merchant financing solutions as well (as they fully own the business data of its merchants).

Beyond e-commerce merchants, small business lending can also come by means of a SaaS-first followed by financing approach. Globally, we see this through companies like Shopify and Toast — which created differentiated SaaS businesses that kick-started a business model driven by high-retention, high-margin subscription software followed by lending (enabled by the transaction / operations data that was now visible through the small business using SaaS). Mekari in Indonesia is an example of a SaaS company that has expanded its services to offer financing through Mekari Capital.

Given again that all small businesses are different, having visibility on real-time operating data (in a way that is easy for business owners) enables lenders to capture niche markets for financing. In my view, small businesses operating in sectors like global trade are pretty interesting and are still under-tapped for both an operating and financing opportunity for FinTechs to serve (see FinKargo in LatAm for example). Imagine being able to build a financial OS for niche small businesses to conduct their financial activity in an integrated way: giving business owners access to new insights on the cash needs of their businesses, getting access to the right capital at the right time, and using it in a way that maximizes their operational potential.

While offering most holistic business services solutions offer one the ability to observe business operations and underwrite based on more exclusive data points (especially if its targeted towards a niche), one cannot force-fit this approach. Almost all of the hyped FinTech companies backed by mega funds like Sequoia and Tiger trying to build point solutions rolling up to financing for micro-scale businesses like warungs (small street shop in Indonesia) ended up dying out or are still suffering from losses in 2023: Ula, Lummo, Bukuwarung. What made Toast work was that its solution was robust and deeply useful on its own. Forcing small business owners to adopt a SaaS platform for the purpose of understanding operations for better underwriting will not work given downstream effects of low retention, usage, without the benefit of the compounding benefits that users enjoy when both financing and operating software integrates deeply with one another.

One can also differentiate based on distribution. Amartha, for example, specialized in funding women-led businesses through partnerships with community partners in rural cities. While traditional micro-finance did not work for them, moving towards a P2P-model with scaled, effective collections allowed them to be profitable for the past four years (from a brink of almost shutting down).

Unit economics and path forward

There are four major buckets of unit economics that cut across both consumer and business financing to keep in mind. Breaking these down from first principles will allow us to understand what the path of optimization looks like and where FinTech can truly add differentiated value:

Acquisition: the cost to market and convince them to apply for a loan.

Underwriting & servicing: the operational costs to evaluate an applicant and, if they are approved, to service their loan

Losses: the cost of absorbing credit risk and fraud losses.

Capital: the cost to acquire the capital to fund the loans.

All the costs are interrelated. The better underwriting and servicing processes are, the lower losses are likely to be. The lower losses are, the lower cost of capital (if raised from external investors) is likely to be. And so on.

FinTech innovation has a role to play in meaningfully lowering these costs. We’ve explained the necessity of these pillars across both consumer and business financing above, but it’s important to restate these again.

Acquisition

Ultimately, lending companies who are able to build moats around acquisition will win — given especially also because financial products are not exactly winner-take-all (a loan from business A vs. business B is hard to differentiate between). A business needs to be strategic and rigorously experimental to find the highest-value channels.

One way to tackle the acquisition problem is through partnerships and embedded distribution, for instance through commerce channels. Koinworks in small business lending shown below has done a great job of doing so. In consumer financing, Paylater firms that are aggressive in acquiring merchant partners in an intentional way (e.g. to capture prime, high-income customers) will build a rich repository of customers that they can bring to other merchants, creating a flywheel.

The other is through a strong wedge. The example of Toast I mentioned who created a differentiated, high-retention SaaS product for restaurants and F&B businesses that led into financing is a great showcase of this. We can apply the same principle to consumer financing. For instance, Finku in Indonesia, originally a PFM-app focused on budgeting and expense management rolled out FinFund: allowing its ~1M users to apply for cash loans through the PFM app itself.

Underwriting & losses

Especially to tackle subprime or thin-file for consumer financing, or to tackle small business lending — one must be “hungry for data” to be utilized for underwriting. Programmatic access to data is now available (e.g. credit bureaus) but Indonesia is still far-behind in terms of access to broader datasets. For instance, cash flow underwriting is difficult as access to both consumer and business bank accounts is difficult. Open banking providers like Brankas and Brick operate on a “gray area” given regulations haven’t exactly given their full blessing and providers like these sometimes use methods such as scraping to obtain the datapoints. This is unlike the United States or the UK where regulators are pushing for open banking, enabling account aggregators like Plaid to provide seamless and trusted access to data from almost all banks. Thus, lenders with access to or are able to create privileged data-sets (like the Advance Intelligence Group example I shared above) find themselves in a strong position.

For small business lending, this is especially important due to the heterogeneity problem where differences in industry or geography significantly impact how to analyze a small business’ creditworthiness. One can tackle this through a wedge or through ecosystem partnerships (like Koinworks does). However the infrastructure to enable MSME lending at scale is still quite nascent. Unlike the US where providers like Rutter, Codat or Railz offer seamless integrations into sales/performance data or accounting data — this does not really exist yet in Indonesia which problem is also accentuated with low uptake of SaaS in Indonesia as compared to developed markets (due to lower labor costs and maturity).

Capital

In order to lend, a FinTech must acquire capital to deploy. Debt capital is getting more expensive to raise in a rising rate environment (government hiked rates twice this year already in Indonesia). Building a trusted, long-term relationship with a bank partner is another approach, although requires a prolonged sales cycle (and the bank partner has leverage in negotiations to push for a higher margin). The longer approach is to intake deposits to minimize cost of capital (being a bank) which leads us well into our next FinTech sector: consumer digital banking or neobanks.

Consumer digital banking (“neobanks”)

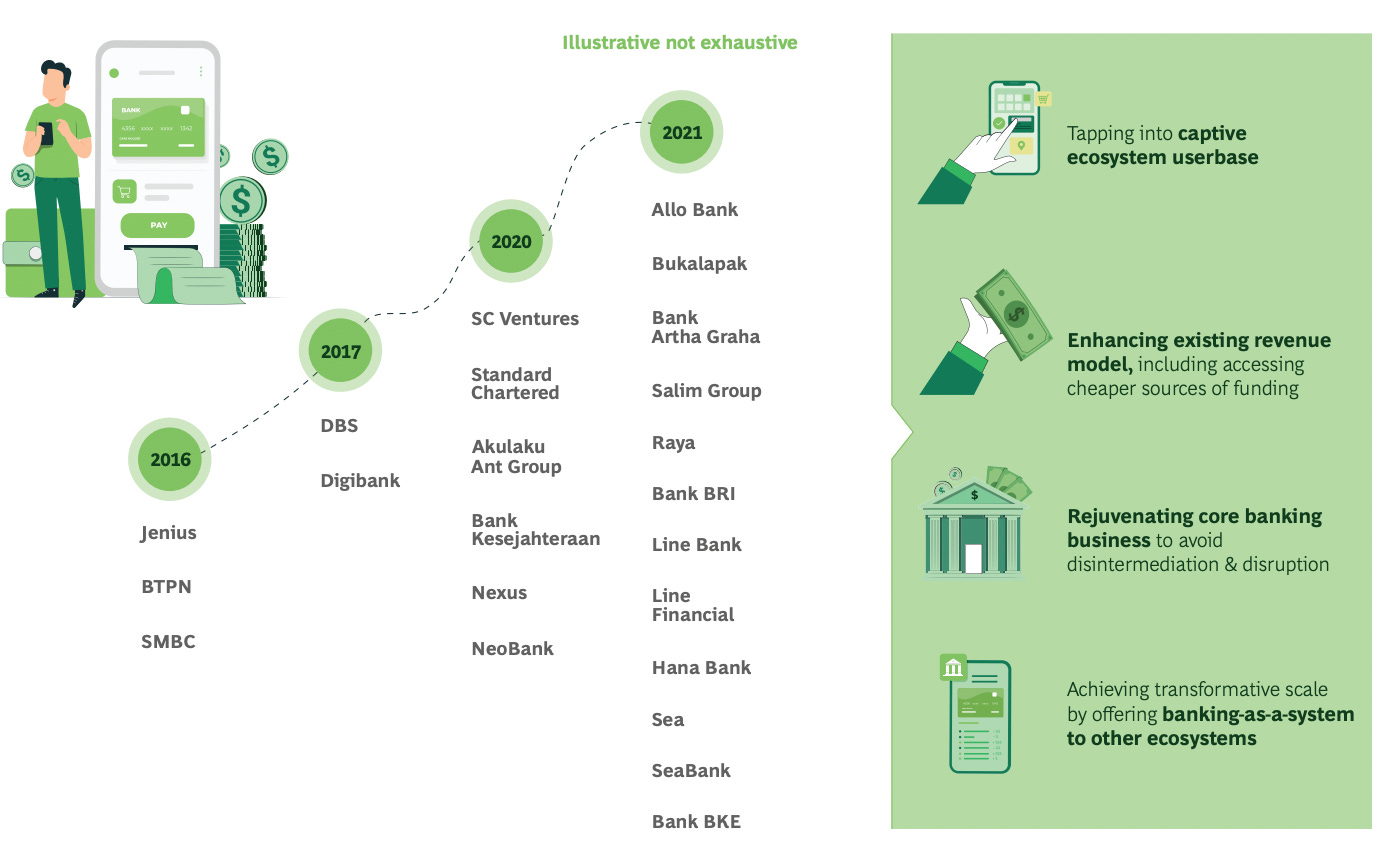

Digital banks were all the rage in the COVID-fueled zero-interest rate policy (ZIRP) era, with smaller banks getting snapped up by well-capitalized players. Consumer lenders took majority stake in banks (Kredivo-Krom, Akulaku-Neo Commerce), small business lenders took stakes in banks (Investree-Amar, Koinworks-BPR Asri Cikupa Karya), and super-app platforms took stake in banks (Sea Group-BKE, Gojek-Jago, Bukalapak-Allo, Grab-Fama). Further, traditional banks BRI and BTPN have rolled out digital banking businesses of their own: Bank Raya and Jenius respectively. You can see the growth of digital banking in the chart above (produced by AC Ventures and BCG). As stated by the report, these digital banks have seen strong growth over the past few years: SeaBank saw 207% YoY growth in total assets in 2022 (to $1.4B), Jago’s customer numbers rising 71% YoY to reach 2.3 million in 2022 with $500M in loan disbursements.

What we have not seen too much as compared to developed markets like the US are niche consumer neobanks tackling very specific segments (from LGBTQ+ to military to creators). This is due to still immature banking-as-a-service infrastructure coupled with a low banked population with equally low financial literacy. According to Euromonitor, the banked population in Indonesia (including the underbanked) is roughly around ~60% in Indonesia vs. ~80% on average across Southeast Asia (besides Singapore). This is due to a higher rate of rural population (~40% of Indonesia) coupled with a relatively higher cash economy, though this is changing.

There are a few players that are targeting niche banking services like Pocket (a family money management platform partnering with Bank Artha Graha International that allows families to open checking accounts with transactions trackable in-app). However, these are not proven yet to work and have seen difficulties even in the United States with their business models (with a few shutting down in 2023).

Despite this, I still believe in the potential of the niche neobank business model if they are able to nail a niche in deep need for differentiated financial services that can generate strong additional revenue beyond deposits (e.g. the elderly).

Let’s start our discussion of consumer digital banking of the benefits one gains from operating their own digital banking platform.

The benefits of owning a bank

There are two archetypes of digital banking players that we see in Indonesia (as mentioned the archetype of niche neobank is not really seen here yet):

Smaller banks acquired by FinTechs / super-apps and converted to digital banks

Established banks who open digital banking businesses / arms

Why FinTech companies or super-apps with FinTech arms (like GoTo Financial) acquire smaller banks to build a digital bank is for two main reasons: (1) to build more holistic financial services and hence generate stronger retention and lifetime value for its end customer, and (2) to reduce cost of funds as it is able to put its own deposits to work. These are both reasons that make absolute sense, although the barrier to entry to conduct such activities is extremely high given the high capital requirements needed to acquire a significant stake in a bank (Gojek paid $159M to acquire 22% of Bank Jago, Grab paid $35M to acquire 16% of Bank Fama, Akulaku paying $10M to acquire 9% of Bank Neo Commerce). If one has a scaled financial services business (most of these acquisitions came up at Series C/D and above), this can make sense economically. However, this strategy is not even close to viable for companies without the level of scale and capital availability.

Established banks building digital banking businesses also makes sense given that most consumers are already used to digital onboarding (internet access penetration in Indonesia at 89% for urban and 74% for rural in 2023) and best-in-class user experiences from the available technology applications and platforms in market. We see an example in the United States of how an established bank Citizens’ Bank implemented “neobank features” (2-day early access to paychecks, less punitive overdraft) to its checking products resulting in higher customer satisfaction and retention in the quote below:

Traditional banks are catching fast in-terms of user experience, with the perceived gap of FinTechs over banks on key dimensions not being significantly wider (banks are more trusted in terms of security, while FinTechs are stronger in terms of access to additional financial services). While FinTechs are able to move fast, banks have the benefit of longevity, well-capitalized war-chests, and trust to sustain and “copy” the successes of challenger models.

My view and that of AC Ventures and BCG is that traditional banks, which have established longstanding and trusted relationships with customers, will continue to play a dominant role in the financial industry. Most consumers still view banks as a preferred channel for both deposits as well as investments. According to ACV’s report, consumers tend to place more assets in banks, with the portfolio value of customers in banks being 6.6 times that of fintechs for average deposits, 2.3 times for interest-bearing deposits, 1.7 times for mutual funds, 2.6 times for Indonesian stocks. While neobanks are catching up with banks in terms of fund transfer frequency and volume, the average deposit in banks is still 6.6 times that in neobanks.

Relationship banking, with the distribution of physical bank branches, has been the focus of established banks since its inception. The roles of branches might still be important to retain deposits especially In a National Bureau of Economic Research working paper titled, “Bank Branch Density and Bank Runs,” researchers point out that banks that spend money on technology tend not to spend as much money building branches and that those banks have a more difficult time holding on to deposits. Their point is stated below:

“Lower branch density allows banks to attract deposit flows and expand funding capacity. However, low branch density also lessens the value of the bank-depositor relationship—shifting the depositor base to corporations and tech-savvy depositors with large, mostly uninsured deposits. These changes to the composition of the depositor base turn out to be detrimental during market downturns: banks with lower branch density experience larger deposit outflows and worse stock performance.”

It’s so hard to quantify the importance of these relationships, but perhaps neobanks will be able to replicate the “core” of this in ways that don’t require branches. For example, LLMs could facilitate dialogue and personalization in a way that previous chatbots could not. Niche neobanks focused on specific segments could build sticky communities of people to facilitate and guide one another.

In order to compete with traditional players, neobanks need to explore new ways to attract and retain deposits. FinTechs and digital banks need to create an enticing proposition beyond offering a superior customer experience and attractive rates in order to capture a higher share of deposits. For the super-apps, this might mean accumulated rewards on transactions on its platform. For pure lending FinTechs, it might mean deeper access to financing with better pricing, or capturing deeper niches (e.g. rural customers). Nubank with their banking services was known to be differentiated due to phenomenal customer service, seamless digital product experience, and best-in-class deposit rates.

Unit economics and path forward for neobanks

There are really three general line items that are important when it comes terms to being a consumer bank (given the broad range of services that being a bank entails):

Customer acquisition costs: the cost to market and convert to a customer

Customer servicing costs: the cost to service a banked customer (e.g. deposit cost)

Customer lifetime value: the revenues accrued from all the banks’ activities (from interchange revenue, value-added services, lending revenues if they do so, etc.)

Customer acquisition costs are an important line item, given the fact that digital banking products are naturally not a product that benefits from organic virality and network effects (unlike let’s say social products like Instagram where users share content with others to generate constant buzz). Given the saturation of existing public channels (e.g. social media), one needs an edge on distribution in order to tackle the acquisition cost hurdle. This is where established banks win with pre-existing relationships with their customers — offering a pathway to those they know already benefit from their services. Super-apps like GoTo and Shopee also benefit in this aspect, as they have large captive audiences that they can promote to with closed ecosystem incentives (like promotions on ride-hailing).

Customer servicing costs are important to consider given a raising rates environment which increases the costs of deposits (customers have safer, higher-interest options — hence there are flights away from the zero-cost deposits or “golden deposits” of the COVID era). Established banks spend a lot of money on their branches (which greatly increases overhead and labor costs), and as mentioned above it is for good reason. Given the war for deposits in an environment where deposit retention is key — the way neobanks can differentiate on servicing so while keeping costs lower will be key (perhaps through enabling technologies like large language models).

Customer lifetime value is the revenue a bank is able to make on its customers. Lending is one way to do so (and hence why so many companies that do have the ability to lend are acquiring banks in order to keep their cost of funds low). However, diverse revenue streams from serving deeper money problems (like wealth or insurance) are also important. For niche neobanks, solving money-adjacent problems can also be a way to drive up value: for instance, a neobank specializing towards the elderly could build value-added fraud protection or even legal services like will-writing or asset insurance.

This philosophy of focusing on jobs to be done for specific segments leads us well into our next conversation on personal financial management platforms.

Personal financial management (PFM)

Personal financial management, or PFM apps, are any product that helps customers get more utility out of the money they already have while doing less work (in this case, I don’t bucket neobanks or consumer wealth here). It’s a broad definition, but one of the important things to note is that PFM is a broad category beyond just what we think as expense management and budget categorization. Here are a few examples:

Budgeting, goals, planning – helping customers understand and control their spending and set short-term and long-term financial goals. In Indonesia, Finku and Sribuu are good examples of this.

Building Better Financial Habits – training customers, through rewards and challenges to develop more financially healthy habits. Cred and Cheq are good examples of this in India — giving rewards for those who pay off credit bills;

Wealth generation – aggregating and recommending opportunities for customers to earn more money, based on each customer’s unique earning situation, and tracking net worth. PINA is a good example of this.

Financial Coaching – helping customers better understand their relationship with money and developing a more productive financial mindset. PINA again is a good example of this, with partnerships with financial coaching communities.

Automated Saving – setting aside money for customers to save without requiring them to do much (or any) work. Digital banks do this well, with Bank Raya’s digital savings product auto-debiting from one’s balance to savings according to a committed plan.

Tracking and Improving Credit Scores – keeping track of customers’ credit scores and providing them with advice on how to improve it. Credit Karma is a good example, which inspired Skorlife in Indonesia.

Debt Resolution – helping customers get out of bad debt through consultation and negotiations with lenders. Amalan is an example of this.

Finding Better Financial Products – recommending financial products that will provide a superior outcome (lower costs, greater rewards or yield, etc.) for customers compared to what they are using today. Cermati is a good example.

The point is: PFM is an extremely broad space and there are still many entrepreneurs building companies for this. In the US alone (from an article by Alex Johnson), you can see that there has not been any slowing down of entrepreneurs building in the space — from the inception of the frontrunners Mint to more new-aged PFMs leveraging new technologies like CoPilot.

The recent news of Intuit shutting down Mint, one of the forerunners of the PFM space, sparked heated discussions on whether or not PFM works. In Indonesia as well, we saw Sribuu shut down recently in 2023 and pivot to SME financial management (the app is still running, but its role in building a venture-backed enterprise is not).

The question is really this: Are PFM’s a standalone business model that can work without add-ons? There are different opinions over here.

Some people believe PFM probably cannot stand alone as a venture-backed business. As a bootstrapped application (like Buddy or Money Lover) that charges people on a subscription basis, it might work. It’s extremely important to have full clarity about how you’re building your business.

Some people believe that PFM can work as key wedges of a broader business model (although again, the risk here is in attempting to force-fit something that inherently is not value-accretive to end users).

Some people believe that new technologies like AI and open banking will make PFM viable as a venture-scaled business (and there are companies attempting to build products in this space that are interesting — for instance, an Indian PFM app called Kniru that has trained a custom LLM for personal finance with a reinforcement learning layer).

15% problem and rethinking PFM business models from first principles

As someone who heads a PFM product, the 15% problem is very real: the fact that only a very small percentage of the general population (15%) enjoys building budgets, categorizing expenses, seeing detailed cashflow patterns, or even monitoring their credit consistently. This will never get meaningfully bigger.

Building off of this, there is no PFM tool for all consumers. Even if you avoid the fifteen percenters, it’s incredibly difficult or even impossible to design a successful mass-market PFM product. Different customer segments need different capabilities, and people are very specific on things like money management.

The better way to embed PFM in my opinion (where I agree again with Alex Johnson) is solving horizontal problems for very specific life stages of people. This will also help overcome the 15% problem for most PFM apps. This is described in the graph below, with PFM apps in the United States segmented into different segments of life categories (the start, the middle, and the end).

The critical resource for consumers at The Start of their financial journey is knowledge. They don’t know how to think about budgeting or the implications of how their decision affect their long-term. They don’t understand how to build a positive credit history. They don’t know how long it will take to save for a down payment for a house or how impactful compounding interest can be on their financial future. People at this stage need help to get off on the right foot and develop the awareness to build up good habits.

Building a PFM application in this case can lead onto other products: imagine a product that helps recent college graduates with holistic financial coaching, management, and habit building in one place: What are the right benchmarks to follow? What is creditworthiness and how to build it? How to sort out taxes, and how should one think about building up one’s income? These are all jobs to be done (following Clay Christensen’s framework) that follow the same thread.

The critical resource for consumers in The Middle of their financial journey is time. They have at least some knowledge of how finance works, and they have likely accumulated some financial assets as well, but they almost assuredly lack the time necessary to manually optimize their short-term and long-term financial outcomes. Those in Indonesia also get married much earlier (25-26 being the average age) meaning they increased responsibilities earlier on in their life.

They want help getting the most out of their money without spending too much of their time. Anecdotally I’m in this segment, and the last thing I want to do on a weekend after a tough week of work and taking care of family is to be on an Excel or an app to crunch/analyze my spending. I do enjoy investing and so don’t need a robo-advisor working on my behalf, but hate that my financial activities reside on different platforms and I have to do the manual math to understand my wealth. For the lower income who are managing multiple loan payments on multiple platforms, this may mean making it easier to “compile” in one go as Cheq does below.

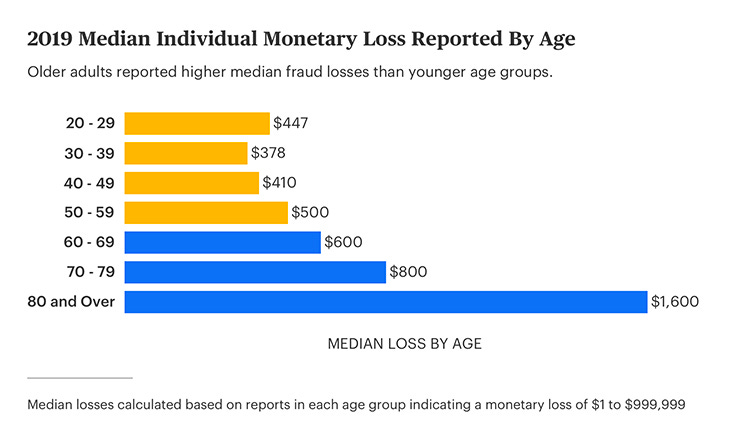

The critical resource for consumers at The End of their financial journey is safety. They have more money and more time available to manage their finances, but they also have much more complex financial situations (e.g. significant assets like property and multiple vehicles). They are also more likely to be dealing with medical challenges that might impair their ability to manage their finances, a fact that fraudsters and unscrupulous companies will constantly seek to capitalize on. They want help keeping themselves and their loved ones’ futures safe. The below chart shows that elderly individuals are more likely to have bigger monetary losses. It represents the condition in the United States, but I would assume the same principle applies to any other country including Indonesia.

I have not seen any elderly-focused startups in Indonesia, and I feel like this is still a very strong blue ocean to build a technology business out of. Carefull is a company focusing on this segment in the United States recently closing a $19M Series A. Carefull’s solution is using AI to scan customer financial accounts to identify activity indicative of financial exploitation. Its models claim to be able to identify behavioral and anomalous financial patterns, which are then flagged for the user or financial institution. Beyond algorithmic monitoring, Carefull also assists with negotiating and canceling bills, performs identity and credit monitoring, and reviews home titles quarterly to identify fraud and tampering.

Open banking and data aggregation problem

Open banking and data aggregation is the foundation that most of the companies in the PFM space rest upon. However, in Indonesia this capability is still extremely nascent, coverage is limited, and ways to extend this coverage cross a regulatory “gray area” given the necessity of using scraping methods with user entering their account details on a different application. I’ll dig into this later in the Infrastructure section, but the inability of PFM apps to safely, compliantly, and seamlessly access account data makes it difficult to perform automated tracking, updates, and analysis to create impact for the end user. Given this, PFM as a category is still slightly impaired in terms of what it “could be”. One passionate about this space needs to be patient for the regulators to start pushing for open connectivity in the financial ecosystem. As Gavin Tan, CEO of Brick (an open banking startup) states: “Regulations are not a hindrance but they’re also unclear – Indonesia is more a case of benign neglect, which can leave doubts about what authorities might do later.” Bank Indonesia has started to roll out and make mandatory open API standard for payments, so an open ecosystem may soon be on the way. But again, patience will be a virtue here.

Infrastructure

Giants cannot be built without leveraging the work of the ecosystem around them. Nowhere is this truer than in fintech, where the complexity of products necessitates partnerships and collaboration across diverse players in the space. If a lending company for instance needed to build their own KYC, build a fraud intelligence and e-KYC system from scratch, operate their own in-house collections team, build their own CMS/LMS — it would be nigh impossible to launch in a way that enables rapid innovation and iteration. The availability of infrastructural players in the space especially today is one of the enablers of the “rebundling”, multi-product thesis I mentioned in the beginning of this article. I hope this can help accelerate understanding of current available infrastructure to leverage and potential opportunities to build in the infrastructure space.

KYC (Know-your-customer)

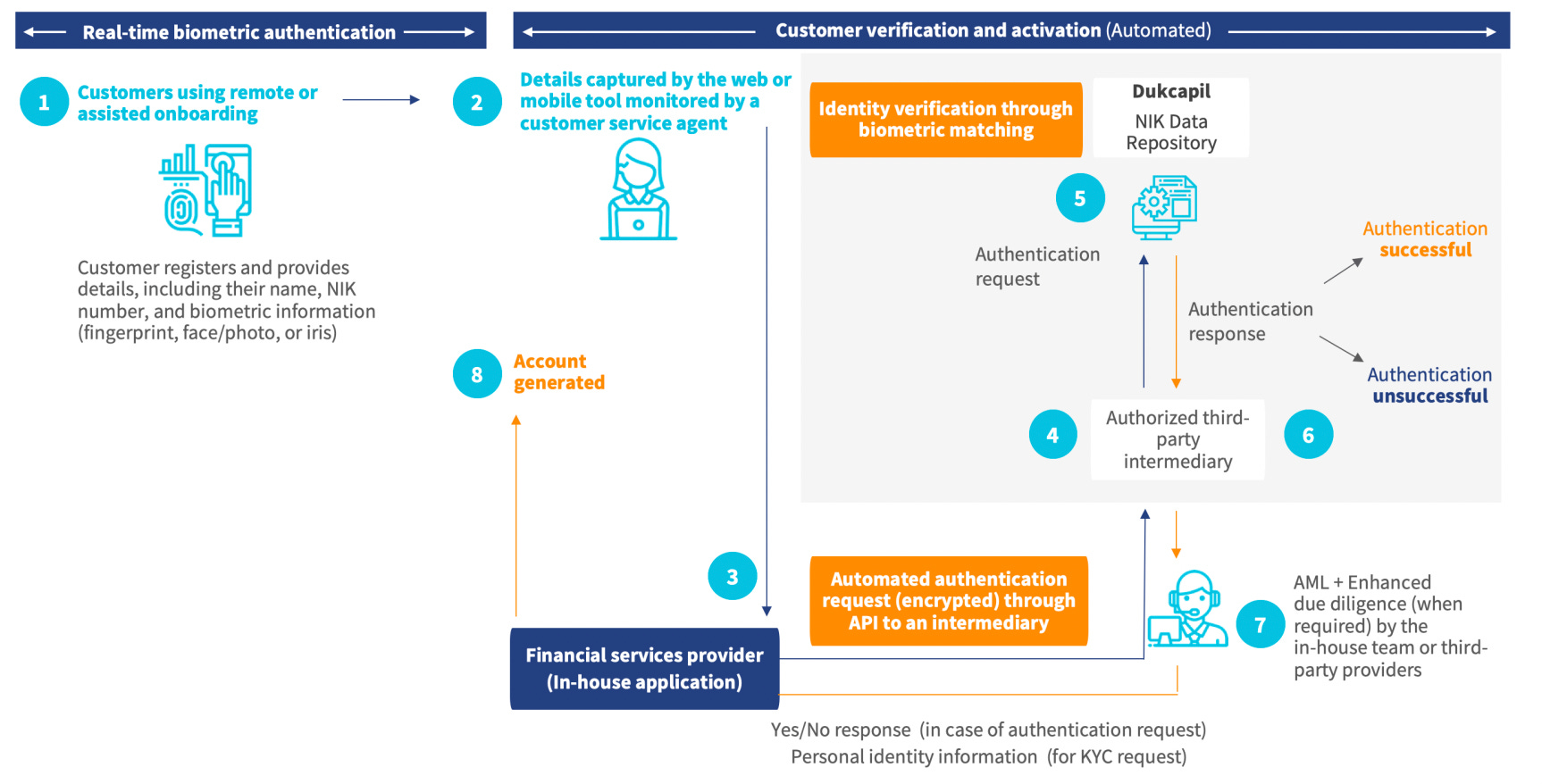

Public infrastructure for E-KYC provides multiple benefits over traditional paper-based KYC. It enables efficiency gains in terms of time, cost, and resource requirements involved in the verification of the identity of an individual or entity. This ensures a near real-time onboarding of a customer for any financial product or service which is needed for many FinTechs.

The Indonesian Financial Services Authority (OJK) established the eKYC (Electronic Know Your Customer) process as a compliance requirement to ensure that financial institutions can efficiently and accurately verify their customers' identities. It has certified a few providers as PsRE's (Penyedia Sertifikat Elektronic) namely players like VIDA, Privy, and Tilaka, who are certified to issue digital signatures verifying that an individual has completed the strict eKYC requirements.

Generally speaking, e-KYC follows the following steps:

A user writes down their particulars (NIK number, name, and date of birth) in app

User then proceeds to take a live selfie (usually with the KTP ID card in frame)

The provider would first do a “Liveness” check on the selfie to ensure that the picture captured is live (which is why some players can also have this be captured in the form of motion capture).

If it passes the Liveness check, the data is then sent to Dukcapil (Directorate General of Population and Civil Registration) to verify for “Demographics” and “Facematch” — where the NIK, name, DOB, and selfie are matched against each other to ensure that it’s the right-fit person.

Only if all these checks pass is the user then issued a digital signature verifying that their identity verification process is complete

The e-KYC process is quite complete right now, although the main challenge in this is still the fact that it relies upon access to a public institution (Dukcapil) database which sometimes faces challenges with downtime. In addition, Dukcapil institutes a hefty $0.3 charge to use its e-KYC services, which adds to the already expensive fully-loaded onboarding costs.

Fraud / AML

FinTech fraud is growing, especially as black-hat hackers get more proficient in getting past e-KYC, getting access to one’s account details (e.g. credit card) which is called ATO or Account Takeover fraud, or tricking one to make a payment to a fraudulent address (APP or Authorized Push Payment fraud) which is much more prevalent now due to real-time payments. In Indonesia, digital financial services fraud has been increasing according to PPATK (Financial Transaction Reports and Analysis Centre), from 9,801 fraud-related suspicious action reports in 2019 to 13,338 in 2020, to approximately 23,000 in 2021.

Players like SHIELD for instance use an SDK to predict how one’s behavior of going through onboarding might indicate fraudulent behavior (based on where one clicks, the speed at which they go through onboarding). Players like Advance Intelligence Group have fraud intelligence products one can embed to monitor against potentially fraudulent transaction history. Large banks and FinTechs should build their own fraud teams to safeguard against these risks as well, but at the very least there is out-of-the-gates infrastructure to help FinTech startups kickstart this work.

Credit bureau + Alternative data providers

As I wrote about in a previous deep-dive on the credit bureaus and the debtor database ecosystem in Indonesia, there is a robust centralized debtor database in Indonesia maintained by the regulators called SLIK. Roughly ~80 million of the 200 million working adults in Indonesia have a credit record in the database. In addition, there is a FinTech Data Center operated by the P2P association AFPI currently that has records of all the alternative lending activities being conducted by P2P platforms. The three credit bureaus in Indonesia starting in 2024 will have access to both these datasets enabling them to have coverage of a wider-set of users including the subprime who have no access to formal credit. From a foundational perspective, Indonesia has the basic building blocks to build lending which is great.

However, as we talked about in the sections on consumer and business lending — lenders are built from the strength of their underwriting and hence must be hungry for more datasets. There are multiple other external sources that one can leverage, although one must conduct proper POCs to ensure that they actually work:

E-commerce data providers like Tokoscore who builds pseudo credit scores, income prediction, and address verification products for users who transact on the GoTo platform

Telco providers who use bill repayments to generate a pseudo score

Mobile data providers like MobileWalla or CredoLab that provide variables about one’s location and other variables (like the # of ATM centers near the vicinity) that might indicate factors like one’s income.

Fraud data providers like SEON that scan multiple sources to check whether one’s credentials have been suspected of previous fraudulent activities

Open finance providers who connect to systems like BPJS (tax) in order to conduct more robust income verification

There are quite a variety of out-of-the-box alternative data providers available, although one has to be intentional of using them given the cost implications (some of these are very expensive) and potential spurious correlation.

Open banking + Banking-as-a-service

As mentioned, open banking capabilities are still quite nascent in Indonesia given that the regulators haven’t forced their hand yet on banks to make their data open (only a select few banks are integrating with open banking providers — and I’m sure the job of those like Brick and Brankas is not easy). Banks are rightfully guarded about this given that these are “their” depositors and data. Thus, it will require regulators to really drive on this to make this infrastructure widely available.

Given the fact that we are still in the data aggregation and payments connectivity steps in open banking — it is still a while until we see core banking-as-a-service infrastructure be developed. Certain banks like BRI and DBS are doing the work by themselves to partner with fintechs and make their systems open for use via API. However, regulatory approval does take time for this and we are still in the nascent stages. Given that banks are not yet at this step, BaaS platforms that facilitate the relationship between the bank and the FinTech similar as what we see in the US (like Unit, Synapse, or recently acquired Bond) are still not yet ready to be built in Indonesia as a proper business.

What we will also likely see is that down the line (although the road here is still further ahead), FinTech companies wanting to tap into BaaS capabilities will want to use more flexible, more powerful core systems to power its use cases (e.g. loan management system, card management system). It’s what we see in India with companies like CARD91, and in the United States with companies like Marqeta. Technical founders might want to keep a close eye on this.

Collections

In order to service FinTechs lenders, collections agencies are required to be registered in AFPI (the FinTech association) to ensure proper compliance and oversight (especially given that collections is traditionally seen as a service that employs “harsh” methods to conduct). And collections is definitely an important infrastructural element of the FinTech ecosystem given that loan book growth is predicted to grow 25% YoY up to 2030, alongside the absolute quantum of bad debt. FinTech lenders can choose to house their own collections team, though this is not the most recommended decision given that this can grow very fast (Kredivo manages 1,000+ agents purportedly). Given this, there needs to be an ecosystem of collections agencies ready to help FinTech lenders minimize the damage from their bad debt. In fact, players like Indodana purportedly use 10+ agencies at one time.

New-age debt collections companies registered in AFPI like Flow, Collectius, MBA Consult provide debt collections outsourcing services to lending companies — everything from banks to multi-finance to FinTechs. They also buy bad debt at a discount to help lenders maintain healthy balance sheets to the regulators. Instead of the traditional “call and shout” or “bang on the door and threaten” approaches — they use data & analytics to segment customers and adjust communications to them based on the receptivity of the segments. Collectius and Flow even build their own debtor portals for borrowers in bad debt to pay off their bad debt in a self-serve manner (this is only when the bad debt is already transferred).

For lenders that decide to manage their own collections team, SaaS providers like Credgenics (a well-funded Indian collections company), Quiros, and Intellix provide systems that lenders can leverage to self-serve. These are complete with integrations to auto-dialers, communications modules through SMS/Whatsapp, and an agent CMS to upload and look at customer profiles.

Next: Wealth/investments, business banking, payments, insurance (COMING SOON - stay tuned!)

For those who reached the end — I sincerely hope that this deep-dive helped you! Can’t wait to bring more impact through the next one. See you soon, and have a great week ahead!